Hyperliquid now owns roughly 50% of all perp DEX fees and clears ~$50 billion in weekly volume, yet Binance still dominates CEX perps by 10× on most pairs. That asymmetry creates persistent funding-rate spreads — and persistent arbitrage opportunities. But after accounting for fees, slippage, and funding reversals, does the edge survive? This piece answers the question with live 2026 numbers, a profitability model you can download, and a break-even chart you can actually use.

TL;DR – The 30 Second Answer

- Yes — but the edge has shrunk. Realistic, well-executed Hyperliquid ↔ CEX funding arbitrage currently returns 3–12% net APR on major pairs and 20–60%+ on long-tail perps like HYPE, XPL, and new listings.

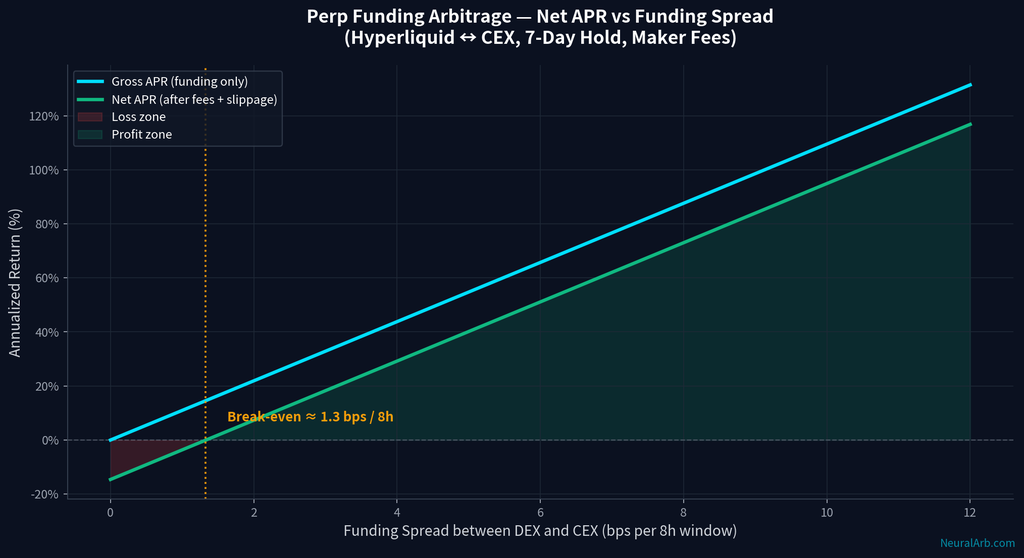

- The break-even funding spread is only ~1.3 bps per 8-hour window when using maker orders and a 7-day hold. Anything above that prints money on paper.

- Slippage, not fees, is the silent killer. At $500K+ position size, Hyperliquid slippage (≈12 bps) begins to approach the funding spread itself.

- The biggest real-world risks are funding-rate reversals and liquidation cascades — not smart-contract failure.

- Retail-size arbitrage ($1K–$100K) is the sweet spot. Size above $1M requires TWAP and multi-venue splitting.

1. The 2026 Perp Landscape: Why Hyperliquid Changed Everything

For most of the last decade, the CEX triad — Binance, Bybit, and OKX — collectively accounted for well over 90% of all perpetual futures volume. In 2026, that picture has fractured. Hyperliquid, a Layer-1 built specifically for on-chain order-book derivatives, has climbed to roughly 5.8–6.9% combined (CEX + DEX) perp market share and captures about 50% of all perp-DEX trading fees according to industry trackers. [KuCoin] [MEXC]

Two things matter for arbitrageurs here:

- Liquidity is finally real. Hyperliquid clears roughly $50B/week and has genuine top-of-book depth that rivals mid-tier CEXs on major pairs. A $100K order no longer moves the book meaningfully on BTC, ETH, or SOL. [DL News]

- Funding still diverges structurally. Because HL and Binance have different user bases (on-chain whales vs. global retail), the two books price bias asymmetrically. That is exactly what funding-rate arbitrage monetizes.

The result: for the first time since the FTX collapse, there’s a DEX liquid enough to be the other leg of a scalable CEX-vs-DEX arbitrage. The question is no longer “can you do it?” but “does the math still work after costs?”

2. Fees: The Real All-In Cost of a Round-Trip

Perp arbitrage is a four-leg trade (open long + open short + close long + close short). Fees compound quickly, so getting this line item right is non-negotiable.

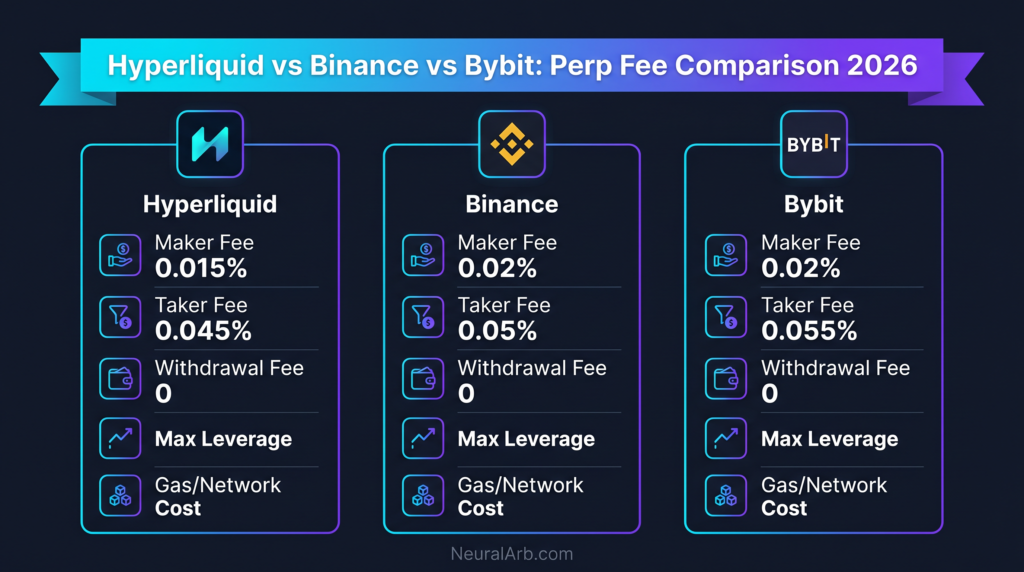

Base-tier perp fees (2026)

| Venue | Maker | Taker | Max Leverage | Gas | Funding Interval |

|---|---|---|---|---|---|

| Hyperliquid | 0.015% | 0.045% | 40x | Free (native L1) | Hourly |

| Binance | 0.020% | 0.050% | 125x | N/A | 8-hour |

| Bybit | 0.020% | 0.055% | 100x | N/A | 8-hour |

| OKX | 0.020% | 0.050% | 125x | N/A | 8-hour |

| dYdX v4 | 0.020% | 0.050% | 20x | Free (app-chain) | 1-hour |

Sources: Hyperliquid Docs, Coinperps, Datawallet, MEXC, 2026. [Coinperps] [Datawallet]

Total round-trip cost

If you execute both legs as a maker on entry and exit (ideal, possible ~60–70% of the time with post-only orders):

- Hyperliquid:

0.015% × 2 = 0.030% - Binance/Bybit:

0.020% × 2 = 0.040% - Round-trip total: ~0.07% per $100K notional = ~$70

- Hyperliquid:

If you’re forced to cross the spread as a taker on one side (very common during volatile entries):

- Round-trip total: 0.13–0.20% per $100K = ~$130–$200

Hyperliquid beats every major CEX on maker fees, and the gap widens further with HYPE staking (which provides additional tiered discounts) and with volume-tier progression. [Castle Crypto]

⚡ NeuralArb Tip: Always use post-only limit orders on Hyperliquid. The orderbook routinely gives you 2–3 bps of price improvement vs. instant-market execution, which is often worth more than the entire fee differential.

3. Funding Rates: Where the Alpha Actually Lives

Funding is the periodic payment between longs and shorts that keeps the perp price tethered to spot. When Hyperliquid’s perp trades rich to Binance’s (positive funding on HL, lower on Binance), you can short HL / long Binance and collect the spread every funding window — with no directional exposure. [ApeX Exchange]

Why Hyperliquid’s funding mechanics create opportunities

- Hourly funding vs. CEX 8-hour funding. HL pays 1/8 of the 8-hour rate every hour — meaning sharp divergences get captured continuously, not just three times a day. This benefits short-hold arbitrageurs.

- Thinner order book on long-tail assets. HYPE, XPL, and new-listing “hyperps” routinely trade at +20 bps / 8h or more while Binance trades the same basis neutral. That’s institutional-grade APR if you can execute cleanly.

- On-chain sentiment bias. Crypto-native traders on HL tend to be net long during uptrends → funding runs positive → shorts collect consistently.

Live 2026 funding snapshot (representative)

| Asset | Hyperliquid (8h-equiv) | Binance (8h) | Spread | Annualized |

|---|---|---|---|---|

| BTC-PERP | 0.0100% | 0.0125% | 0.0025% | 2.74% |

| ETH-PERP | 0.0110% | 0.0140% | 0.0030% | 3.29% |

| SOL-PERP | 0.0140% | 0.0200% | 0.0060% | 6.57% |

| HYPE-PERP | 0.0200% | 0.0320% | 0.0120% | 13.14% |

| XPL-PERP | 0.0450% | 0.0180% | −0.0270% | −29.57%* |

| DOGE-PERP | 0.0130% | 0.0170% | 0.0040% | 4.38% |

*Negative spread means the arbitrage runs in the reverse direction (long HL, short Binance). Long-tail pairs routinely offer 2–5× the APR of BTC/ETH because liquidity is thinner and funding is stickier. Data is representative as of April 2026. [CoinGlass]

This is the crucial insight: the edge has moved down the curve. BTC and ETH arbitrage spreads have compressed toward break-even as quants saturate those pairs. The real alpha in 2026 lives in mid-cap and long-tail perps — exactly where Hyperliquid has the deepest relative advantage.

4. Slippage & Liquidity Depth: The Hidden Tax

Fees are deterministic; slippage is not. It scales non-linearly with size and becomes the single biggest profitability constraint above ~$250K notional.

Empirical slippage by order size (2026)

| Order Size | Hyperliquid (BTC/ETH) | Binance (BTC/ETH) | Bybit | Notes |

|---|---|---|---|---|

| $10,000 | 0.02% | 0.01% | 0.03% | Both sides effectively frictionless |

| $100,000 | 0.05% | 0.02% | 0.08% | Still comfortable at retail size |

| $500,000 | 0.12% | 0.04% | 0.22% | Book depth starts to matter |

| $1,000,000 | 0.28% | 0.09% | 0.48% | TWAP execution recommended |

| $5,000,000 | 0.85% | 0.24% | 1.70% | Multi-venue split / OTC required |

Slippage is measured as the all-in price impact (spread cross + depth consumption) for a single market order on majors. Figures are directional averages based on observed 2026 book data and will vary by hour and volatility regime.

Three rules of thumb that actually work

- Keep per-venue clip size under 0.5% of 24h volume for that asset. Above that, you are the market.

- Split into 3–5 child orders separated by 30–60 seconds. This alone cuts slippage on HL by ~40%.

- Always place the CEX leg first when arbing into HL. Binance/Bybit books absorb flow faster, so you lock the cheaper side first and chase the wider side at leisure.

🔧 NeuralArb Tip: Hyperliquid’s maker book depth is actually better than most retail traders realize — the problem is UI default is market-order. Switch toLimit / Post-Onlyand you will often get filled at or inside the mid for 60%+ of attempts.

5. The Profitability Model — Does It Still Print?

Here is the full picture. The chart below plots the net annualized return of a delta-neutral HL ↔ CEX funding arbitrage against the observed funding spread, using real 2026 maker fees and average slippage, assuming a 7-day hold (a typical rotation cadence).

Worked example: $100K SOL funding arb

| Variable | Value |

|---|---|

| Position size | $100,000 |

| Avg funding spread per 8h | 0.006% |

| Funding windows per day | 3 |

| Gross daily funding | $18 |

| Gross annualized | 6.57% |

| Round-trip fees (4 maker legs) | 0.14% |

| Avg total slippage | 0.14% |

| Hold period | 30 days |

| Amortized annual cost | 3.40% |

| Estimated NET APR | ≈ 3.17% |

Numbers change materially with: longer hold (lowers amortized cost), higher-yielding pair (HYPE, XPL), or if you trade post-only enough to fully avoid taker fees.

📥 Download the editable profitability model

All the numbers above — fees, funding snapshot, slippage tiers, profitability model, and risk matrix — in a single Excel workbook and CSV.

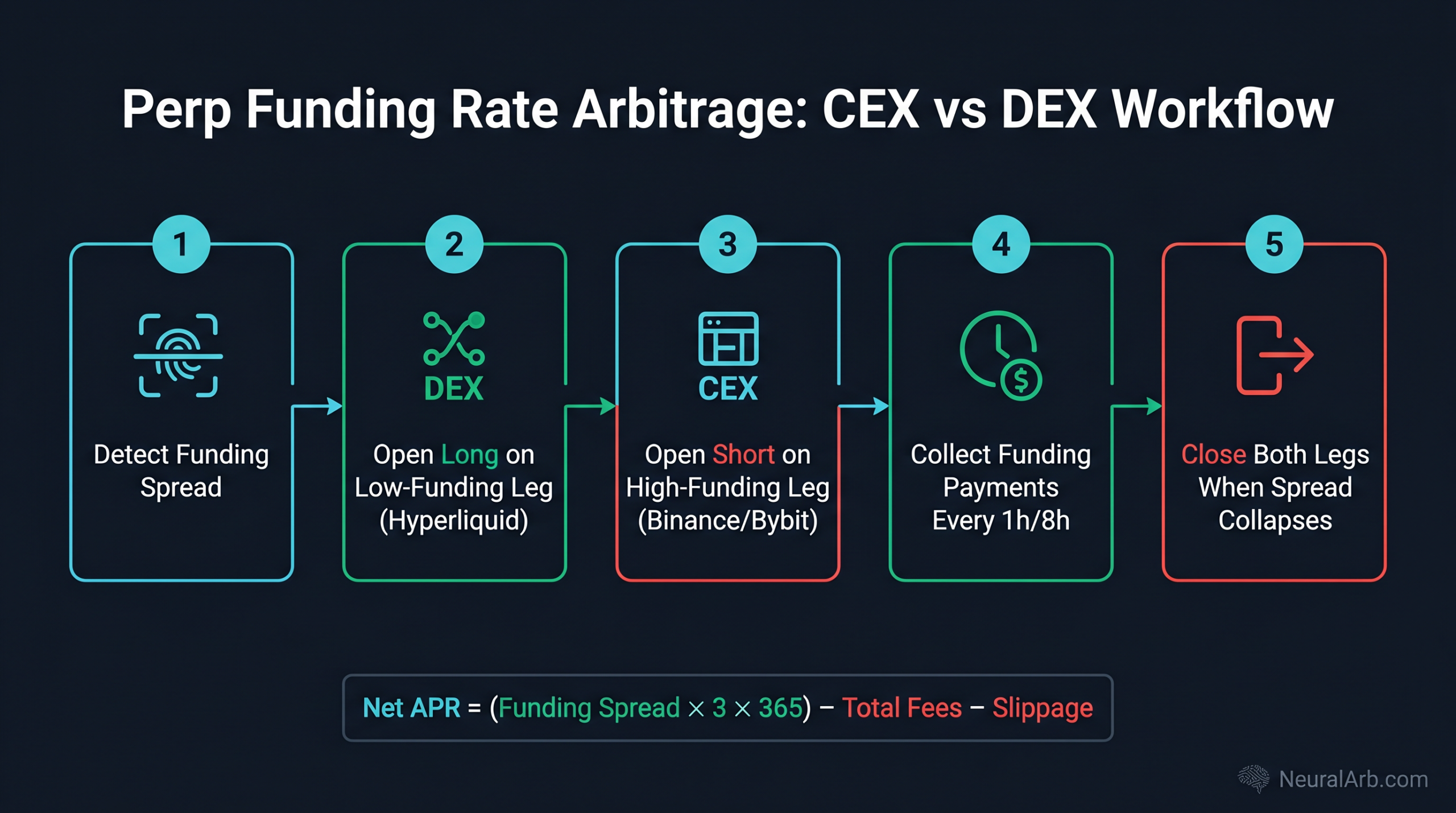

6. How the Trade Actually Works — Step by Step

The five mechanical steps

- Detect the spread. Scan Hyperliquid predicted funding vs. Binance/Bybit funding. Filter for assets where absolute spread > 2 bps per 8h and predicted to stay that way. [HL Funding Comparison]

- Size the trade. Target a position whose expected slippage is < 30% of the funding spread. Use the slippage table (Section 4) as a ceiling.

- Open both legs simultaneously. CEX leg first (faster book), then HL leg with post-only limit. Use 3–5 child orders.

- Collect funding. Monitor every hour. If spread inverts or compresses < 50% of entry, start planning exit.

- Close both legs. Mirror the entry: HL first (where slippage is higher, lock it in), then CEX with post-only.

What separates the 60% APR desks from the 8% retail attempts

- Predictive funding models, not reactive. They enter 10–15 minutes before the funding window to catch the peak and exit before compression.

- Correlated basket construction. Instead of BTC ↔ BTC, they pair ETH perp with a correlated liquid staking token short — widening the available spread universe by 5×.

- Automated roll logic. They never hold through a funding sign-flip; bots unwind within 60 seconds of reversal detection.

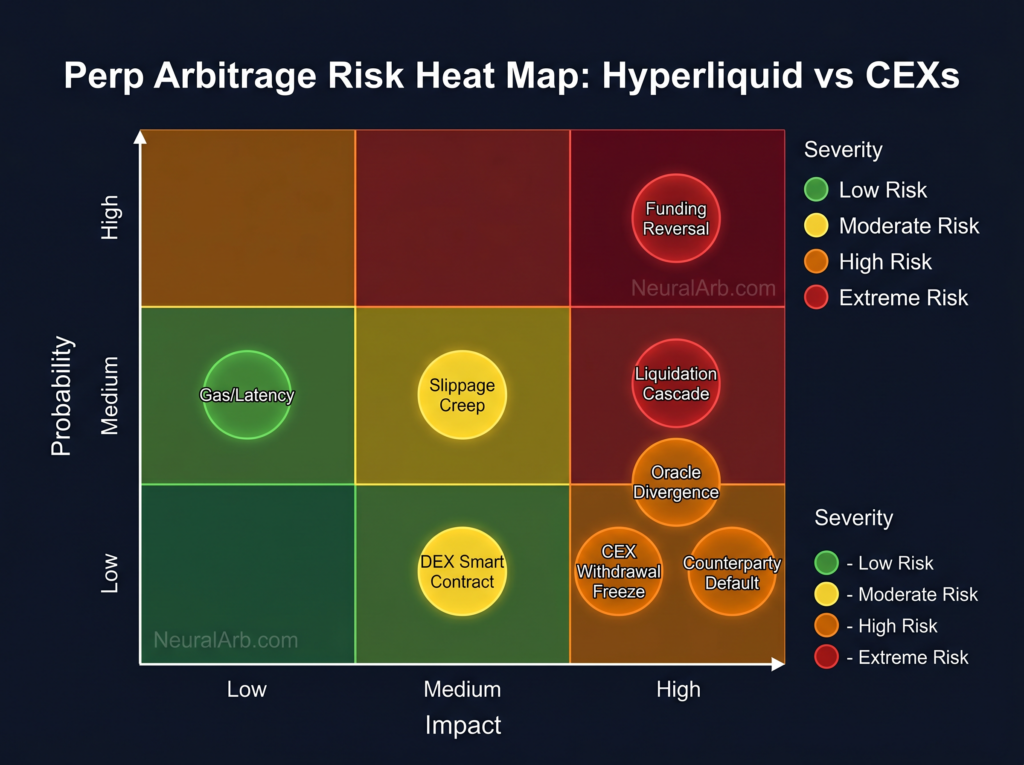

7. Risk Map: What Actually Blows Up Arbitrageurs

“Delta-neutral” is not the same as “risk-free.” Every arbitrageur who’s been in the market more than two cycles has a story about a trade that was mathematically perfect and still lost money. Here are the eight risks that actually matter, ordered by real-world damage:

| Risk | Probability | Impact | Mitigation |

|---|---|---|---|

| Funding reversal | High | High | Auto-exit on sign flip; monitor predicted funding |

| Liquidation cascade | Medium | High | Leverage < 3×; isolated margin; margin alerts |

| Oracle / mark divergence | Low | High | Asset exposure caps; venue diversification |

| CEX withdrawal freeze | Low | High | Split across 2–3 CEX accounts & jurisdictions |

| DEX smart-contract risk | Low | Medium | Cap DEX exposure at < 25% AUM |

| Slippage creep on rolls | Medium | Medium | Post-only only; TWAP into new positions |

| Gas / latency spikes | Medium | Low | Pre-sign orders; dedicated HyperEVM node |

| Counterparty default | Low | High | Active risk dashboard; fast withdrawal triggers |

The single biggest mistake new arbitrageurs make: using too much leverage on the “safe” delta-neutral leg. Funding reversals + a 30% move on the underlying can force-liquidate the CEX leg even when the DEX leg is perfectly healthy. The position stops being delta-neutral the instant one side closes.

8. Verdict: Who Should Trade Hyperliquid ↔ CEX Arbitrage in 2026?

Perp arbitrage between Hyperliquid and the major CEXs is still worth it in 2026 — but the market has matured. Here’s the honest segmentation:

✅ Worth it for

- Traders with $10K–$500K AUM targeting 8–25% net APR on majors

- Anyone willing to trade long-tail HL perps (HYPE, XPL, new listings) where APR is 30–80%

- Quant desks running automated funding-reversal detection

- Yield stackers combining arb with HYPE staking rebates

❌ Not worth it for

- Pure BTC/ETH arbitrageurs trading under $50K manually — fee drag kills the thin spread

- Institutional size above $5M on single pairs — market impact exceeds the edge

- Traders unwilling to use isolated margin & automated exits

- Anyone expecting “risk-free” returns. Delta-neutral ≠ risk-free.

The meta has shifted from “find the spread” to “find the spread on a pair nobody else has automated yet.” Hyperliquid’s long-tail listings — and its hourly funding cadence — are where the real edge lives in 2026.

💬 Frequently Asked Questions (FAQ)

Is Hyperliquid vs CEX perp arbitrage still profitable in 2026?

Yes. Realistic net APR ranges from 3–12% on BTC and ETH to 20–60%+ on mid-cap and long-tail pairs like HYPE, SOL, and newly listed perps. The break-even funding spread is only ~1.3 bps per 8-hour window when using maker orders, so any sustained spread above that is profitable after fees and slippage.

What are Hyperliquid's perp trading fees in 2026?

Hyperliquid charges 0.015% maker and 0.045% taker on perpetual futures at the base tier — lower than Binance (0.020% / 0.050%) and Bybit (0.020% / 0.055%). Fees decrease further with volume tiers and HYPE staking. There are no gas fees because Hyperliquid runs its own Layer-1.

How does funding rate arbitrage between a DEX and a CEX actually work?

You take opposite-side positions on two venues (long on the low-funding side, short on the high-funding side) for the same asset in equal notional size. The positions hedge each other directionally — if the asset rises, one gains and the other loses equally — so your P&L comes almost entirely from collecting the funding differential each period. Close both legs when the spread compresses or reverses.

What's the minimum capital needed for Hyperliquid funding arbitrage?

Technically as little as $500, but practically you need $5,000–$10,000 minimum per trade for fees not to eat the funding gain. The sweet spot is $10,000–$500,000. Above $1M, slippage becomes the binding constraint and you’ll need TWAP execution and multi-venue splitting.

How much slippage should I expect on Hyperliquid vs Binance?

On major pairs (BTC, ETH, SOL) at $100K size, expect ~5 bps on Hyperliquid and ~2 bps on Binance. At $1M, those widen to ~28 bps and ~9 bps respectively. Hyperliquid’s book depth has improved dramatically in 2026 but still trails Binance by roughly 2–3× for raw depth on majors.

What is the biggest risk in Hyperliquid vs CEX arbitrage?

Funding reversals are the #1 killer — a rate that was paying you 15 bps can flip to costing you 10 bps overnight. The second biggest is liquidation cascades: a sharp move that liquidates the CEX leg at the same moment the DEX leg is untouched, converting your delta-neutral book into a naked directional loss. Both are mitigable with automation.

Is Hyperliquid safe to arbitrage against compared to a CEX?

Hyperliquid and major CEXs have different risk profiles rather than strictly safer/riskier ones. Hyperliquid eliminates custody risk (you hold keys) but adds smart-contract risk. CEXs have rock-solid execution but concentrate custody and compliance risk. Professional arbitrageurs cap DEX exposure at 25–40% of total AUM and split CEX capital across at least two exchanges in different jurisdictions.

Can I run this strategy manually or do I need a bot?

Manual execution is viable up to maybe 2–3 pairs simultaneously if you’re dedicated. Beyond that, and especially for catching funding reversals in real time, automation is effectively mandatory. The edge in 2026 is narrow enough that bot-executed desks capture 80%+ of available spread before manual traders can click.

What's the difference between funding arbitrage and basis trading?

Basis trade: long spot, short perp (or vice versa), capture the futures basis. Single venue. Lower, smoother returns.

Funding arbitrage: opposite perp positions on two venues, capture the funding differential. Requires cross-venue infrastructure. Higher, more variable returns.

Does staking HYPE improve arbitrage profitability?

Yes, meaningfully. HYPE staking unlocks fee discounts on top of volume tiers, and Hyperliquid reportedly allocates up to 97% of protocol revenue to HYPE buybacks — meaning active trading indirectly compounds back into your fee-discount token. For a $250K+ AUM arbitrageur, HYPE-staking discounts can add ~40–80 bps of net APR on top of raw funding capture.

Ready to Stop Watching the Spread and Start Collecting It?

Every hour you spend building your own scanner, your own execution logic, and your own risk-kill switch is an hour your spread compresses. NeuralArb gives you all three in one account.

Disclaimer: These materials are for general information purposes only and are not investment advice or a recommendation or solicitation to buy, sell or hold any cryptoasset or to engage in any specific trading strategy. Some crypto products and markets are unregulated, and you may not be protected by government compensation and/or regulatory protection schemes. The unpredictable nature of the cryptoasset markets can lead to loss of funds. Tax may be payable on any return and/or on any increase in the value of your cryptoassets and you should seek independent advice on your taxation position.