TL;DR:

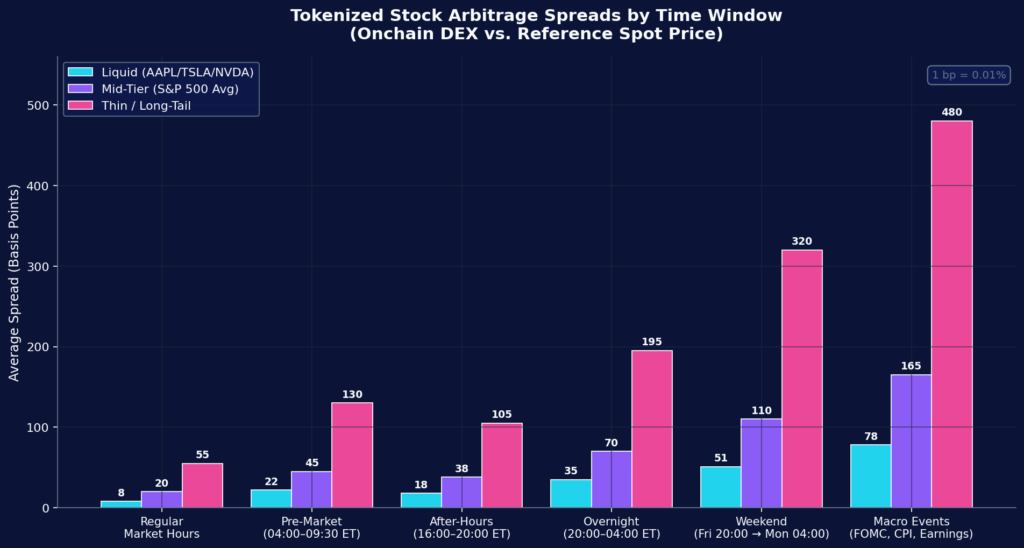

Tokenized stocks are blockchain-issued tokens backed 1:1 by real equities (AAPL, TSLA, NVDA, SPY) that trade 24 hours a day, 7 days a week on Solana, Ethereum, Arbitrum and BNB Chain. Because the underlying NYSE/Nasdaq market is closed ~127 hours every week, onchain prices drift on news, sentiment and liquidity — creating systematic arbitrage windows. Average spreads run 8 bps in regular hours, 35–55 bps overnight, and 51–110 bps over weekends, with macro-event spreads exceeding 200 bps on liquid names. Cumulative tokenized equity volume crossed $39 billion by April 2026, with xStocks alone above $25B. For traders running AI-driven, latency-sensitive infrastructure such as NeuralArB, 24/7 onchain equities offer a higher-frequency, lower-friction arbitrage frontier than traditional market hours equities — but only with proper execution rails, hedging and oracle hygiene.

1. Why “24/7 Stocks” Is the Most Important Market-Structure Shift Since 1985

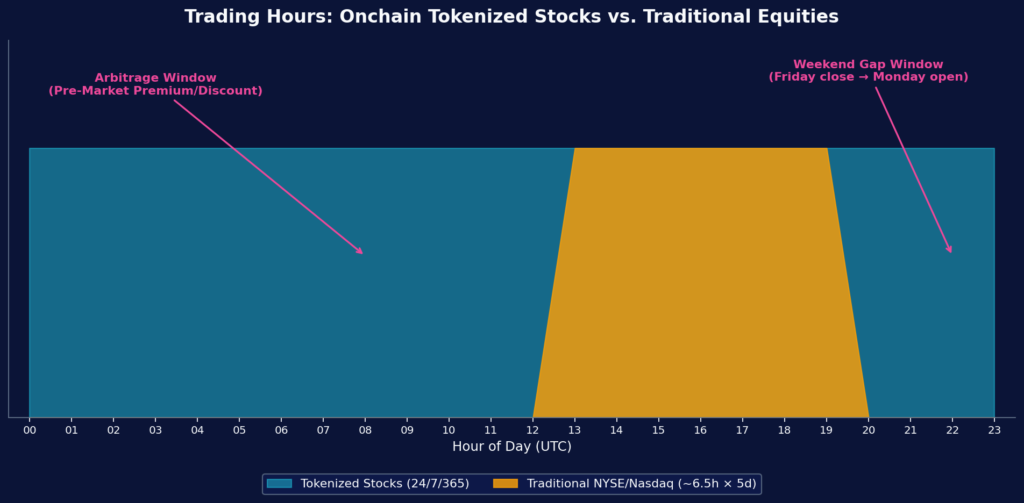

The traditional U.S. equity market is open just 6.5 hours a day, 5 days a week — roughly 32.5 of every 168 hours. That’s only 19.3% of the calendar week. Tokenized equities flip the equation: onchain rails settle continuously, so AAPL, TSLA, MSFT, NVDA and even SPY can change hands at 3 a.m. on a Sunday from a wallet in Singapore.

In 2026, this stopped being theoretical. NYSE announced a tokenized ATS for 24/7 trading, Nasdaq filed a tokenization framework with the SEC, and CME Group launched 24/7 crypto futures [PYMNTS]. On the issuer side, xStocks (Backed Finance/Kraken) crossed $25B cumulative volume, Ondo Global Markets pushed $2B+ tokenized assets to Solana, and Robinhood EU listed 200+ stock tokens on its Arbitrum L2 [The Block].

For an arbitrageur, three structural facts matter:

- Tokenized stocks track — but never perfectly mirror — their reference price. Whenever NYSE is closed, onchain prices float on order-flow alone.

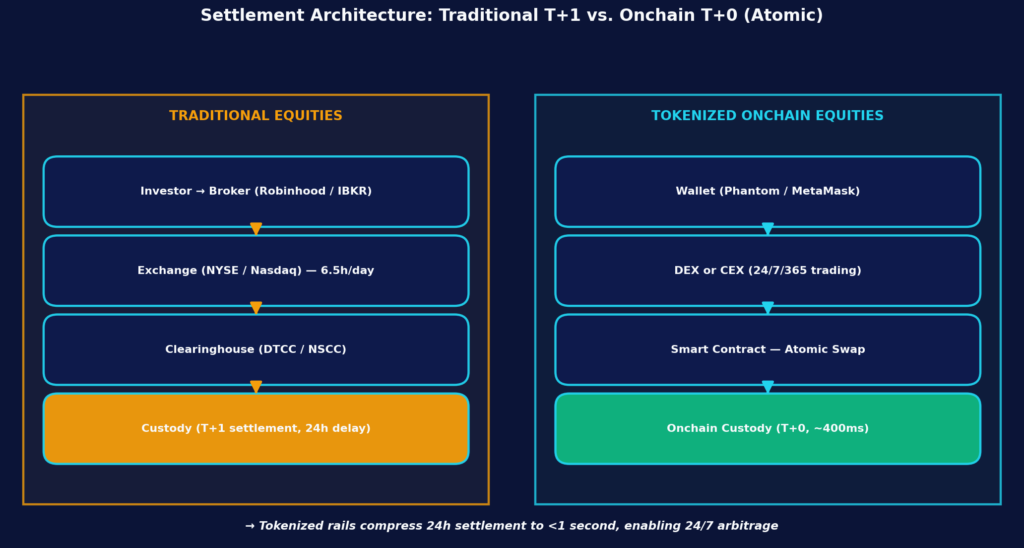

- Onchain settlement is atomic (~400 ms on Solana), vs. T+1 (24 hours) at DTCC. This compresses risk-of-carry to near zero.

- Authorized Participants (APs) can mint and redeem 1:1, anchoring fair value but with friction (KYC, banking hours, redemption windows). Friction = persistent spread = arbitrage.

This article quantifies those spreads, maps the strategies, benchmarks the infrastructure, and gives you a downloadable toolkit to model your own P&L.

🎯 For the Solana-specific deep-dive, see Solana Tokenized Stocks: A New Frontier for High-Frequency Arbitrage.

2. What Are Tokenized Stocks (and Why Arbitrage Exists at All)?

2.1 The 1:1 Backing Model

A tokenized stock is an ERC-20, SPL or similar onchain token whose issuer (Backed, Ondo, Dinari, Robinhood) holds the equivalent share with a regulated custodian — Alpaca holds ~75% of all tokenized stock float [The Information]. Most are structured as derivative contracts referencing the share, which means token holders typically don’t get voting rights, but they do get price exposure plus dividends streamed onchain [PYMNTS].

2.2 Why Onchain Price ≠ Reference Price

Three frictions keep onchain price from snapping perfectly to NYSE:

- Time gap: NYSE is closed ~127 hours per week.

- Capital cost: APs need balance sheet to mint/redeem; they only do so when the spread covers their cost of capital + ops.

- Liquidity fragmentation: AAPL trades on Raydium, Orca, Uniswap v4, Bybit and Kraken simultaneously. Prices reconverge through arbitrage, not by decree.

A peer-reviewed market-microstructure study found tokenized equity spreads run ~51.42 bps on average — roughly 10× wider than traditional equities during overlapping hours [ScienceDirect]. That gap is the opportunity.

3. The Anatomy of a Tokenized Stock Arbitrage Trade

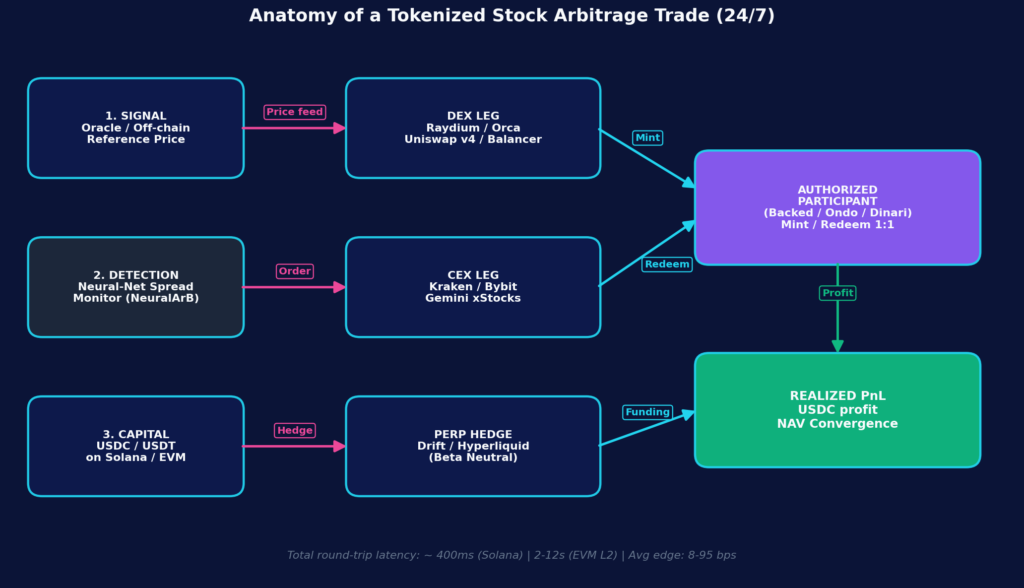

Every onchain equity arb breaks down to four steps: Signal → Detection → Execution → Settlement.

A neural-network spread monitor compares the off-chain reference price (Pyth, Chainlink, broker feed) against onchain pool prices on Raydium/Orca/Uniswap every block. When the spread breaches the cost-of-execution threshold (gas + fees + slippage + funding), the bot fires both legs atomically — buying the cheap leg and selling the expensive leg — and either holds for NAV convergence at NYSE open or hedges with a perp on Drift / Hyperliquid.

This is exactly the architecture NeuralArB’s neural arbitrage engine was built for: sub-second detection, multi-venue routing, and reinforcement-learning-driven sizing.

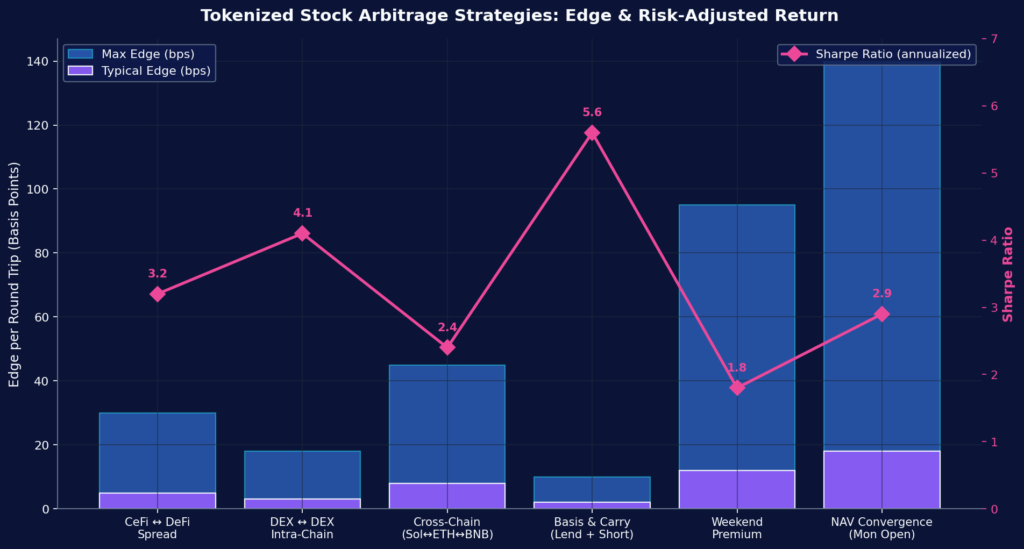

4. The Six Live Arbitrage Strategies (Ranked by Edge & Sharpe)

4.1 CeFi ↔ DeFi Spread (The Bread-and-Butter Trade)

Buy AAPLx on Raydium at $201.20, sell on Bybit at $197.50 (or vice versa). Typical edge: 8–30 bps. Pure latency game; the bot that detects the spread first wins.

4.2 DEX ↔ DEX Intra-Chain Arbitrage

Within Solana alone you have Raydium, Orca, Phoenix, Lifinity, Meteora. A large market order on one venue lifts the price; the others lag for ~200–800 ms. Typical edge: 3–18 bps with very high frequency (40+ trades/day per asset).

4.3 Cross-Chain Arbitrage (Solana ↔ Ethereum ↔ BNB)

Ondo lists tokenized stocks on Solana, Ethereum, and BNB Chain simultaneously [Ondo Finance]. Spreads can blow out to 25–45 bps when one chain’s pool gets temporarily imbalanced. Requires intent-based bridges (Across, deBridge) to rotate inventory in <30 seconds.

4.4 Basis & Carry Trades (Highest Sharpe)

Lend tokenized AAPL on Solend at 2–4% APY, simultaneously short AAPL-USDC perpetual at +0.05% funding. Edge per trade is small (2–10 bps), but the Sharpe ratio is the highest at ~5.6 because the position is delta-neutral and runs 24/7.

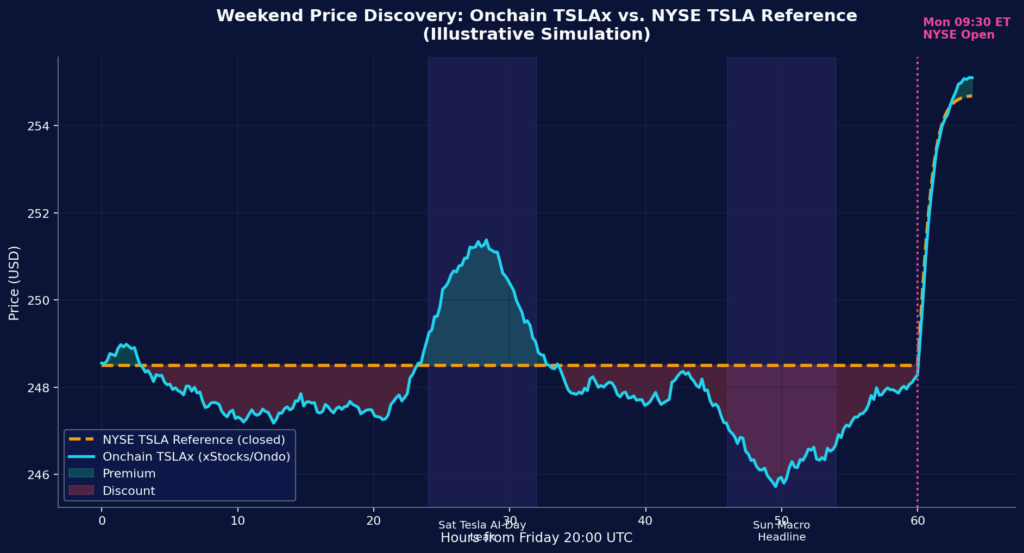

4.5 Weekend Premium Capture (Highest Absolute Edge)

This is where 24/7 onchain equities truly beat market hours. From Friday 4 p.m. ET to Monday 9:30 a.m. ET, the underlying market is closed for ~65 hours. News doesn’t stop:

A Saturday Tesla AI-Day leak or a Sunday geopolitical shock can push tokenized TSLAx 50–150 bps off the Friday close. Typical edge: 12–95 bps, but execution risk is real — your hedge has to wait until Monday open.

4.6 NAV Convergence at NYSE Open

The highest absolute edge of all (18–140 bps). At 9:30 a.m. ET Monday, the NYSE reopens and the tokenized price is forced to converge with the spot. Bots front-run convergence by accumulating mispriced tokens during the last 60 minutes of the weekend window.

🎯 Compare with RWA Arbitrage: Tokenized Treasury Price Gaps for fixed-income equivalents.

5. Settlement Architecture: Why Onchain Wins on Latency, Loses on Depth

The single biggest reason 24/7 onchain equities can beat traditional market hours is atomic settlement. T+1 at DTCC means your capital is locked for 24 hours after every trade. Onchain, the same trade settles in 400 milliseconds.

| Rail | Settlement | Cost / Tx | Trading Hours | Atomic? |

|---|---|---|---|---|

| Solana | ~400 ms | $0.00025 | 24/7/365 | ✅ |

| Arbitrum L2 | ~250 ms | $0.05–$0.30 | 24/7/365 | ✅ |

| Ethereum L1 | ~12 s | $2–$35 | 24/7/365 | ✅ |

| Base L2 | ~2 s | $0.02–$0.10 | 24/7/365 | ✅ |

| NYSE / Nasdaq | T+1 (24h) | $0.03/share | 6.5h × 5d | ❌ |

| NYSE Tokenized ATS (2026) | Real-time | TBD | 24/7 | ✅ |

The trade-off: traditional venues still have 100–1,000× deeper books for liquid names. A $10M AAPL order clears on Nasdaq at <1 bp slippage; on Raydium it eats 30–60 bps. Smart arbitrageurs size to onchain depth and use CeFi venues (Kraken, Bybit) as the deep counter-leg.

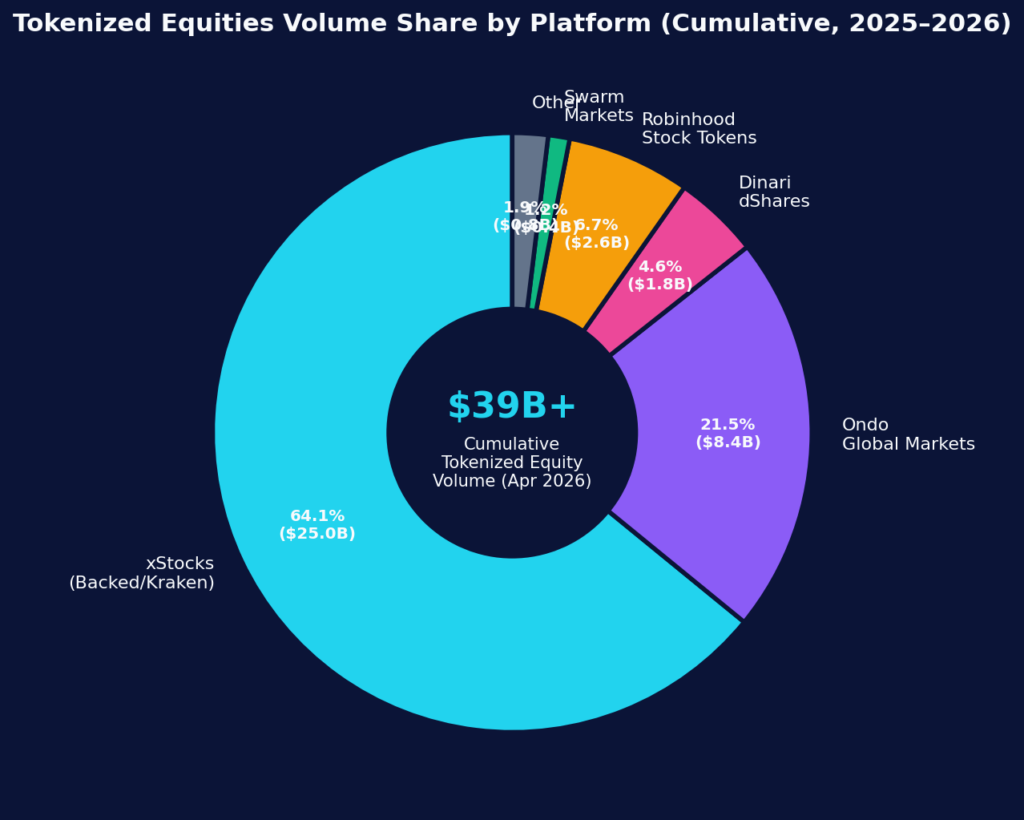

6. Platform Landscape: Where the Volume Actually Lives

Two issuers control ~86% of the tokenized equity market Token Terminal:

- xStocks (Backed Finance / Kraken) — $25B+ cumulative volume, dominant on Solana, available on Bybit, Kraken, Gemini.

- Ondo Global Markets — $8.4B+ across Solana, Ethereum, BNB Chain, with deep DeFi composability.

- Robinhood Stock Tokens — $2.6B, exclusive to EU retail on Arbitrum L2 (24/5, not 24/7) Robinhood.

- Dinari dShares — $1.8B, the only U.S.-regulated issuer (Reg A+).

- Swarm, Mt Pelerin, Coinlocally — long-tail venues with niche listings.

For arbitrageurs, xStocks + Ondo overlap is the highest-quality opportunity surface: same underlying, different chains, different oracle feeds, different liquidity profiles.

7. The Real Risks (And How to Engineer Around Them)

A 51-bp average spread sounds free — it isn’t. Here are the seven risk vectors that destroy unprepared arbitrage strategies:

- Oracle lag / oracle freeze. If Pyth or Chainlink stalls, your “spread” is phantom. Always cross-validate against ≥2 feeds.

- AP redemption gating. Mint/redeem windows close on weekends. You may be unable to crystallize the spread until Monday.

- Liquidity wall. Pool depth at ±50 bps is often <$500K for non-MAG-7 names. Size the trade to depth, not to capital.

- Bridge risk. Cross-chain arbs depend on canonical or intent-based bridges. Use Across, deBridge or LayerZero — never an unaudited custom bridge.

- MEV & front-running. Public mempools leak your trade. Use Jito bundles on Solana or Flashbots Protect on EVM.

- Funding-rate flips. Carry trades reverse if perp funding flips negative during stress.

- Regulatory surface. MiCA passport for EU, SEC no-action for U.S., HKMA/MAS for APAC. Tokenized stocks are not legal for U.S. retail SEC Statement.

🎯 Read our Comprehensive MiCA Compliance Guide for the EU regulatory checklist.

8. So Can 24/7 Onchain Equities Actually Beat Traditional Market Hours?

Short answer: Yes — but only on three dimensions.

| Dimension | 24/7 Onchain Equities | Traditional Market Hours | Winner |

|---|---|---|---|

| Trading availability | 168 h/week | 32.5 h/week | 🏆 Onchain |

| Settlement latency | ~400 ms | 24 hours (T+1) | 🏆 Onchain |

| Cost per tx | $0.00025–$0.30 | $0.03/share + commissions | 🏆 Onchain |

| Liquidity depth (large-cap) | Shallow | Deep | 🏆 Traditional |

| Spread (regular hours) | 8–55 bps | 0.5–3 bps | 🏆 Traditional |

| Spread (weekend / events) | 51–480 bps | N/A (closed) | 🏆 Onchain (only game in town) |

| Arbitrage frequency | 24/7 + macro events | Weekday open/close only | 🏆 Onchain |

| Capital efficiency | Atomic, looped | T+1 lockup | 🏆 Onchain |

The verdict for arbitrageurs: 24/7 onchain equities decisively beat traditional market hours on capital velocity, settlement, and event-driven edge. They lose on raw spread tightness during overlap hours — but that’s irrelevant for the 81% of the week when traditional markets are simply not open.

The math is brutal in onchain’s favor:

- 8 bps × 250 days × 28 trades/day = +560% gross / year on a CeFi-DeFi book.

- 78 bps × 50 weekend events × 4 trades = +1,560 bps of pure event alpha that traditional markets cannot capture at all.

9. Downloadable Toolkit: Run the Numbers Yourself

We built a free, editable Excel workbook with 8 sheets:

What’s inside:

- Overview & navigation

- Market_Cap_Growth — 11-month historical series + auto-chart

- Spread_Matrix — color-coded bps grid by liquidity tier × time window

- Platform_Volumes — share table + pie chart

- Strategy_Calculator — plug-in your capital, edge, win-rate → daily/monthly/annual P&L

- Weekend_Simulation — 64-hour TSLAx vs NYSE reference series

- Cost_Latency_Compare — side-by-side rail benchmark

- Risk_Checklist — 13-point pre-deployment due-diligence sheet

10. Frequently Asked Questions (FAQ)

What is tokenized stock arbitrage in simple terms?

Tokenized stock arbitrage is the practice of buying and selling blockchain-based tokens that represent real stocks (like AAPL or TSLA) across different venues to profit from price differences. Because onchain prices update 24/7 while NYSE/Nasdaq close at 4 p.m. ET, predictable spreads emerge — especially on weekends and during macro events.

Are tokenized stocks legal in the U.S.?

For most U.S. retail investors, no. Issuers like xStocks and Ondo restrict access via geo-blocking. Dinari dShares is the main exception, registered under SEC Regulation A+. Institutional U.S. investors can access tokenized equities via qualified custodians under exemptive relief SEC.

How big is the tokenized stocks market in 2026?

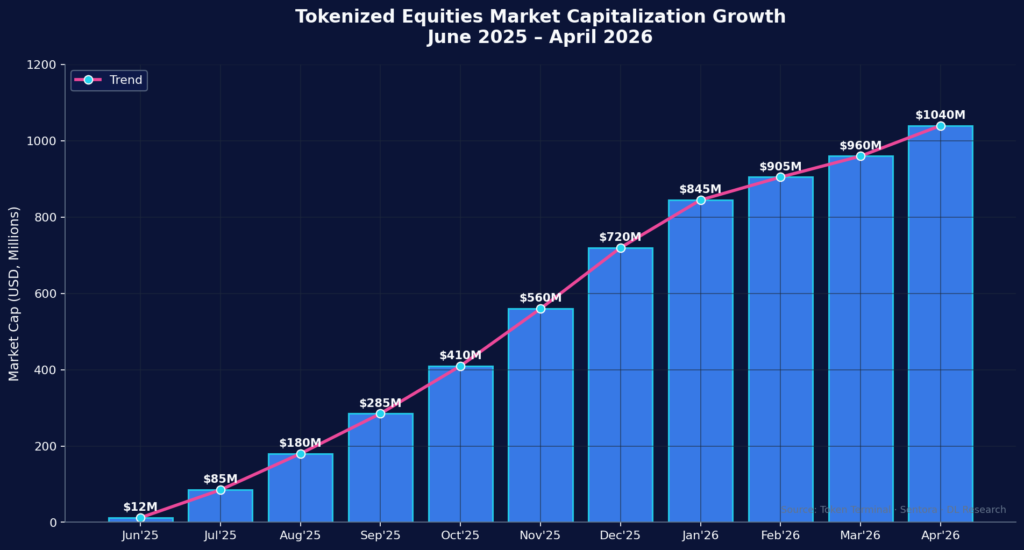

Tokenized equities reached ~$1.04 billion in market cap and $39+ billion in cumulative trading volume by April 2026, growing roughly 80× year-over-year Token Terminal. BCG projects the broader tokenized-asset market could reach $16 trillion by 2030.

What's the best blockchain for tokenized stock arbitrage?

Solana, by a wide margin. Sub-second finality (~400 ms), $0.00025 transaction cost, and ~95–99% of global tokenized equity volume make it the dominant venue. Arbitrum is second for EU/Robinhood flow; Ethereum L1 is too slow and expensive for high-frequency strategies.

How much capital do I need to start?

Strategy-dependent. DEX-DEX intra-chain arbitrage can run profitably from $10K–$25K thanks to negligible Solana fees. Weekend premium capture and basis trades become economic at $50K+. Cross-chain arbitrage needs $100K+ to absorb bridge fees and inventory rotation.

What's the average spread I can realistically capture?

Net of fees and slippage: 5–15 bps per round-trip on liquid names in regular hours, 25–80 bps on weekends, and 50–200 bps during macro events (FOMC, CPI prints, earnings).

Do I need to build my own bot?

You can — but the engineering bar is high (sub-100ms execution, MEV protection, multi-venue routing, oracle redundancy, hedging). Most professional traders use AI-driven platforms like NeuralArB that handle the infrastructure layer end-to-end.

What are the biggest risks?

Issuer solvency (Backed/Ondo/Dinari), oracle freezes, AP redemption gating on weekends, MEV/front-running, regulatory shifts, and liquidity-wall slippage on thin names. The risk-checklist tab in the toolkit walks through all 13 vectors.

How is tokenized stock arbitrage different from crypto arbitrage?

Crypto arbitrage relies on volatility and fragmentation between exchanges; tokenized stock arbitrage adds a predictable closure cycle of the underlying market — a structural inefficiency that doesn’t exist in pure crypto. Returns are also more correlated to equity events than to BTC/ETH cycles, which is excellent for portfolio diversification.

Will NYSE's tokenized ATS kill the arbitrage edge?

Eventually, yes — for regular-hours spreads on liquid names. But weekend, overnight and macro-event spreads will persist as long as the underlying NYSE auction itself is paused. NYSE’s own 24/7 platform launching in 2026 will compress mid-day spreads while creating a new arbitrage axis: NYSE-tokenized vs. independent issuer (Ondo/Backed) prices.

11. Conclusion: 24/7 Stocks Are Not the Future – They’re the Present

The question wasn’t whether tokenized stocks would arrive. It was whether arbitrageurs could industrialize the spread before institutions compressed it. With NYSE, Nasdaq, CME, Robinhood and BlackRock all moving in 2026, the window is open today and narrowing fast. Traders who deploy AI-driven, multi-venue, multi-chain infrastructure now will own the edge for the next 18–24 months — exactly the moment retail and institutional adoption fully ramps.

24/7 onchain equities don’t replace traditional market hours. They add 135.5 hours of tradeable surface every week that simply didn’t exist before — and that is where the alpha lives.

Profitable in Any Market Condition

Join 10,000+ traders using NeuralArB’s neural network technology to profit from market inefficiencies 24/7. Whether the market goes up or down, the spread is yours.

Disclaimer: These materials are for general information purposes only and are not investment advice or a recommendation or solicitation to buy, sell or hold any cryptoasset or to engage in any specific trading strategy. Some crypto products and markets are unregulated, and you may not be protected by government compensation and/or regulatory protection schemes. The unpredictable nature of the cryptoasset markets can lead to loss of funds. Tax may be payable on any return and/or on any increase in the value of your cryptoassets and you should seek independent advice on your taxation position.