TL;DR

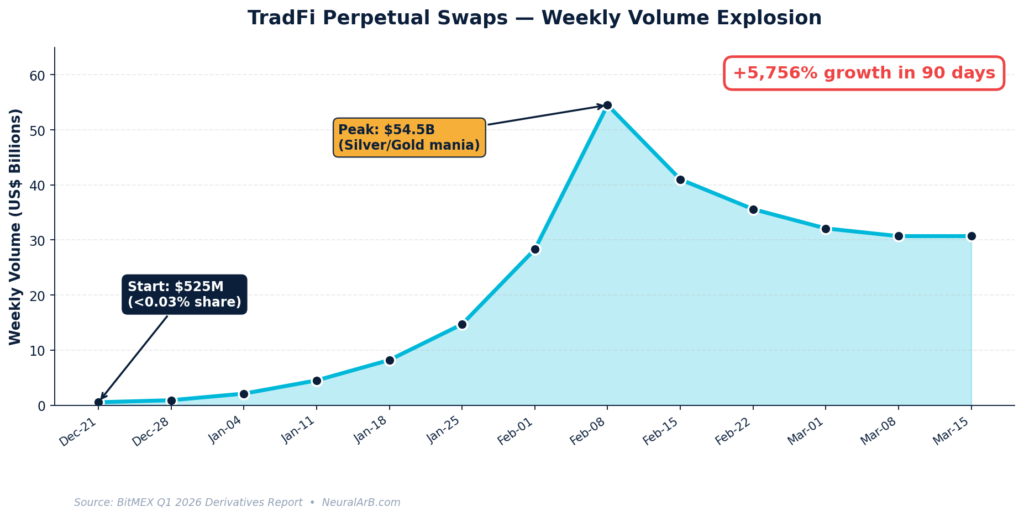

In Q1 2026, weekly volume in TradFi perpetuals (perp contracts on stocks, indices, commodities, and FX) exploded from $525.8M to $30.7B, a +5,756% surge in just 90 days. With Kraken launching the first regulated tokenized-equity perps, Hyperliquid unlocking permissionless HIP-3 markets, and the CFTC opening the door to perpetuals on US soil, the lines between crypto and traditional finance have dissolved. For arbitrageurs, this is the most asymmetric opportunity since the 2020 DeFi summer.

What Are TradFi Perpetuals? A Definition for the AI Era

A TradFi perpetual (often shortened to TradFi perp or RWA perp) is a perpetual swap — a derivative with no expiry date — written against a traditional-finance underlying such as a single stock (TSLA, NVDA), an equity index (S&P 500, NASDAQ 100), a commodity (gold, silver, crude oil), or a foreign-exchange pair. Mechanically it is identical to a Bitcoin perpetual: it uses a funding-rate mechanism to keep the mark price tethered to the spot reference, supports high leverage, and trades 24 hours a day, seven days a week — including weekends and Wall Street holidays.

What makes TradFi perps revolutionary isn’t the financial engineering — perpetual swaps have existed in crypto since BitMEX invented them in 2016. It’s the convergence of three rails that previously could not interact:

- Tokenized real-world assets (RWAs) — issuers like Backed, Ondo, and Securitize now mint 1:1-collateralized tokenized versions of equities and ETFs on public blockchains.

- Perpetual-DEX infrastructure — venues like Hyperliquid, dYdX, Aster, and Ostium can list any market with a price oracle and a small bond.

- Regulated CEX derivatives venues — Kraken’s offshore PDSL entity, Bitnomial (a CFTC-licensed DCM), Binance, and BitMEX are now offering equity/commodity perps under formal supervision.

Stitched together, these three rails create a 24/7, leveraged, capital-efficient market for assets that previously stopped trading every weekend at 4 p.m. New York time. For arbitrageurs, that mismatch is the alpha.

Why TradFi Perpetuals Are Exploding in 2026

The numbers tell the story

According to the BitMEX Q1 2026 Derivatives Report, TradFi perp weekly volume detonated from $525.8 million in late December 2025 to $30.7 billion by mid-March 2026, peaking at $54.5 billion during the silver/gold mania of the week of February 8. Market share inside the crypto-margined derivatives universe jumped from a rounding error (0.03%) to 1.72% in just one quarter (BitMEX).

Binance Research corroborates the trend: average daily TradFi-perp volume across all venues rose 188% from $3B in January to $8.6B in March.

What’s driving the surge?

- Always-on demand for stocks. Retail traders, especially in Asia and Latin America, want exposure to Nvidia, Tesla, and the S&P 500 without waiting for the NYSE opening bell.

- Permissionless markets. Hyperliquid’s HIP-3 framework lets anyone post a bond and launch a perpetual market on any oracle-priceable asset. Open interest on HIP-3 markets has already crossed $2.3 billion, with crude-oil perps leading the pack (Yahoo Finance, CoinDesk).

- A licensing breakthrough. In March 2026, S&P Dow Jones Indices licensed the S&P 500 benchmark to Trade[XYZ] for perpetual contracts on Hyperliquid — the first time the world’s most-traded index has been available as an on-chain 24/7 perp (S&P Global Press).

- A regulatory thaw. The CFTC issued a public Request for Comment on perpetual contracts in April 2025 and subsequently permitted listing of BTC/ETH perpetual futures on regulated US exchanges, signaling that perpetuals are no longer offshore-only instruments (Pillsbury Law).

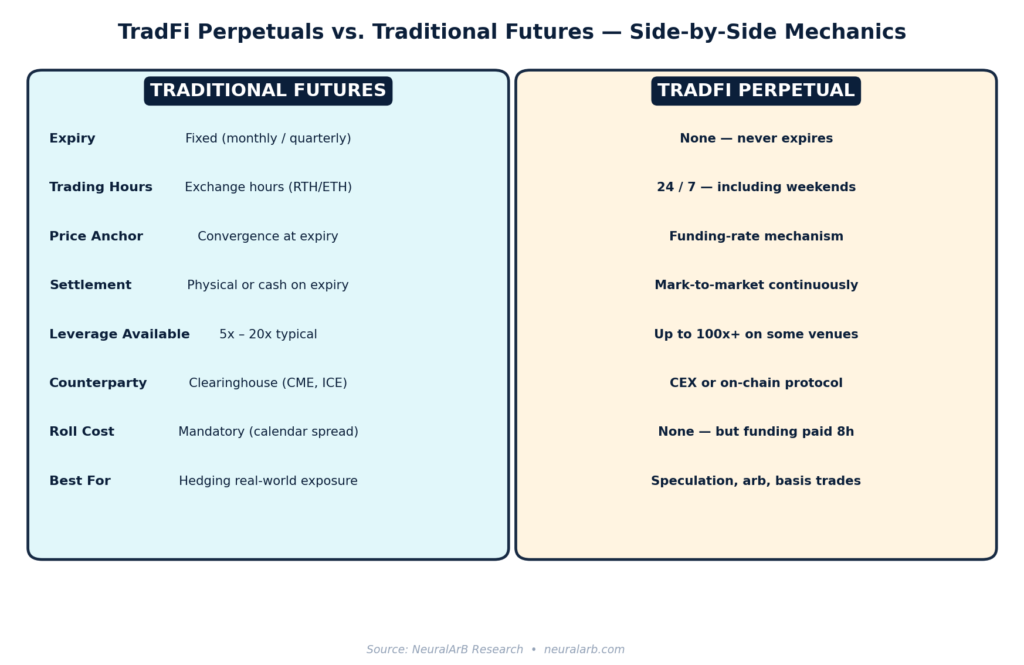

TradFi Perps vs. Traditional Futures: What’s Actually Different?

If you’ve ever traded a CME E-mini or an ICE Brent contract, the perpetual model will feel familiar — but the cash-flow mechanics, hours, and collateral logic are fundamentally different.

The two structures converge on the same economic exposure but diverge sharply on how that exposure is funded and rolled:

- Traditional futures force price convergence through a hard expiry date. If you want continuous exposure, you must roll quarterly and eat the calendar-spread cost.

- Perpetuals never expire. Instead, an 8-hour (sometimes 1-hour or continuous) funding payment flows between longs and shorts to keep the perp price glued to spot. When perp > spot, longs pay shorts; when perp < spot, shorts pay longs.

This single design choice — funding-rate convergence instead of expiry convergence — is what creates the most powerful arbitrage opportunity TradFi has seen in years.

Where the Volume Is Flowing: Exchanges and Asset Classes

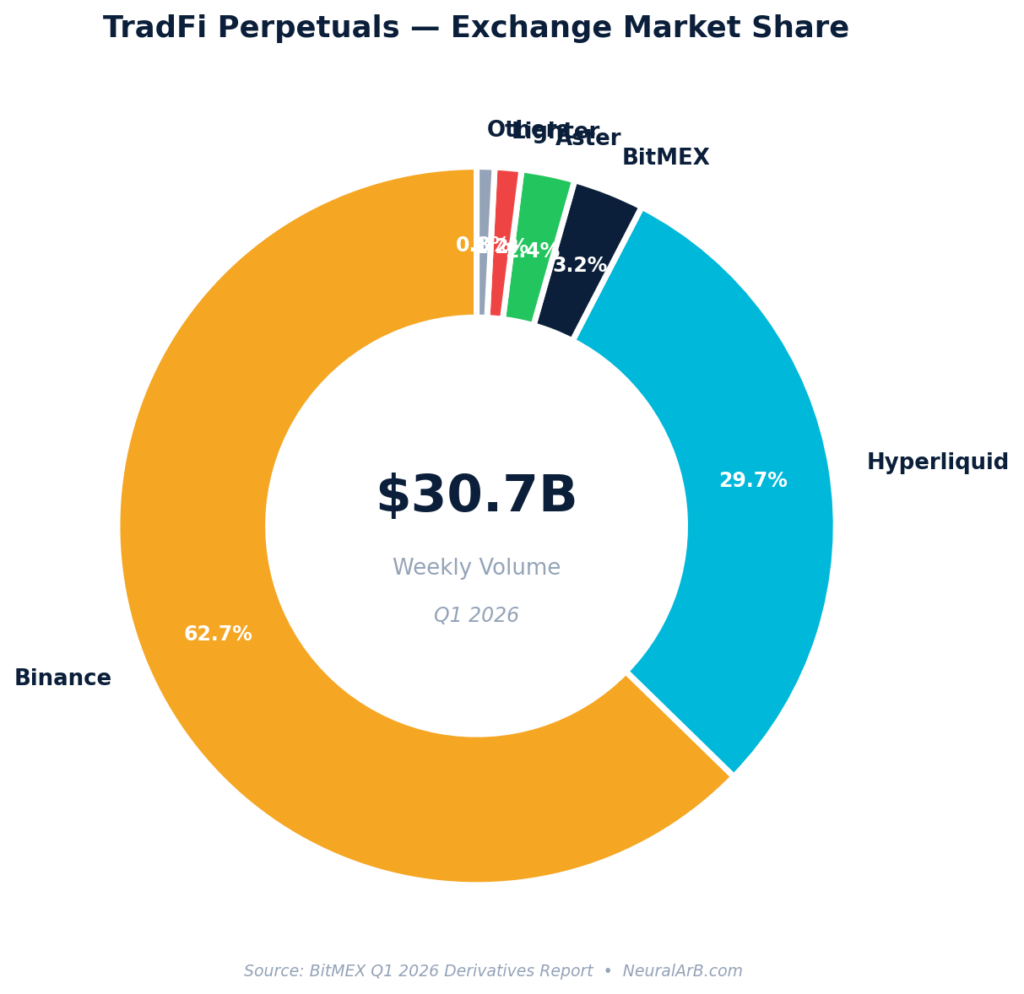

The exchange leaderboard

A single quarter rewrote the league table:

- Binance — exploded into the lead with 62.7% market share after a +74,536% volume surge from a near-zero base (BitMEX).

- Hyperliquid — captured 29.7% thanks to HIP-3’s permissionless market launches.

- BitMEX — the quiet outperformer at +1,322% growth, second-best in the entire sector.

- Aster, Lighter, and others — together hold the remaining ~4%, with Lighter the only major venue contracting (-30.4%).

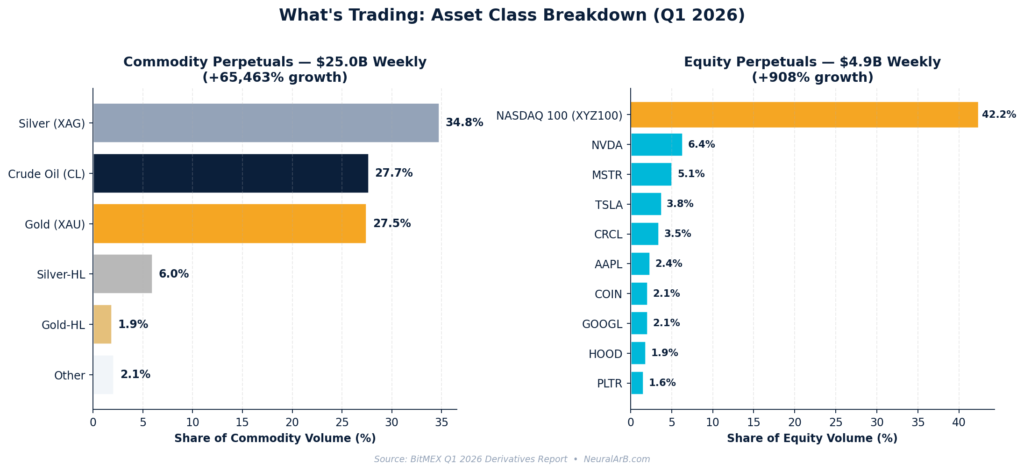

The asset-class breakdown

Commodities delivered the headline number: +65,463% growth to $25 billion weekly, dominated by silver (XAG), crude oil (CL), and gold (XAU) — assets that historically required a futures account and exchange membership to trade with leverage. Equities grew a “modest” +908% to $4.9 billion weekly, with Hyperliquid’s XYZ100 NASDAQ-100 perpetual capturing 42.2% of equity volume. The rest of the top 10 reads like a retail-favorite leaderboard: NVDA, MSTR, TSLA, CRCL, AAPL, COIN, GOOGL, HOOD, PLTR (BitMEX).

The Arbitrage Battlefield: Where Crypto Meets Wall Street

This is the section your trading desk actually cares about. Because TradFi perps run 24/7 on crypto rails while their TradFi counterparts respect Wall Street hours and clearinghouse rules, persistent dislocations appear daily.

Below are the five highest-edge strategies active in 2026, ranked by maturity.

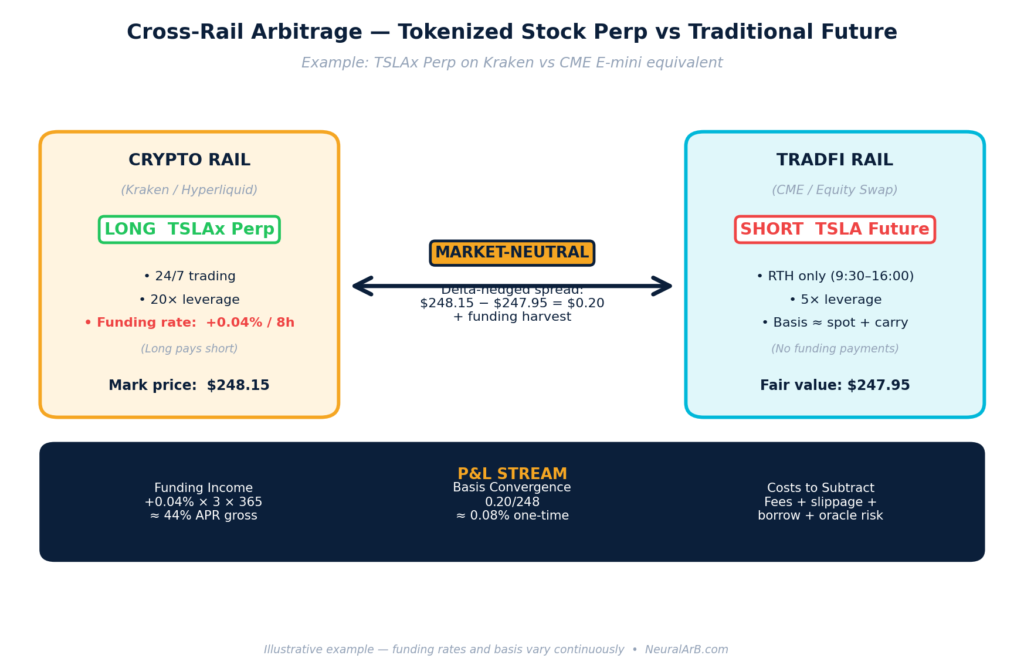

1. Funding-rate harvest (cash-and-carry on tokenized equities)

When the perpetual mark price trades above its TradFi reference for a sustained period, the funding rate goes positive — longs continuously pay shorts. An arbitrageur shorts the TradFi perp and simultaneously buys either (a) the underlying tokenized equity (e.g., TSLAx) or (b) the actual stock via a prime broker. The result: a delta-neutral position that earns the funding spread.

Coinglass and Bitget data show single-asset funding rates frequently exceed 30-50% APR on hot equities during earnings weeks, sometimes spiking to 100%+ during macro events (CoinGlass, Bitget).

2. Cross-venue funding arbitrage

The same underlying — say NVDA — trades as a perp on Kraken, Hyperliquid, Binance, and BitMEX. Funding rates rarely match across venues. A trader can go long the venue paying the highest funding (negative rate, longs receive) and short the venue paying the lowest (positive rate, shorts receive), hedging the directional exposure. This is the foundational play powering desks like NeuralArB’s automated agents.

3. Weekend & overnight basis trading

Tokenized equities and their perps trade through Friday-night, Saturday, Sunday, and US holidays — but the underlying stock market is closed. When macro news breaks on a Saturday, perps reprice immediately while traditional futures gap on Sunday-evening reopen. Sophisticated funds front-run the gap by trading the perp, then close against Monday’s cash open.

4. Calendar arbitrage vs CME / Eurex futures

Traditional futures have explicit term structure; perps embed it implicitly via funding. When the annualized funding rate diverges from the calendar-spread basis on the equivalent CME contract, an arb desk can construct a butterfly across rails — long perp, short front-month CME, long back-month CME (or vice versa). This is institutional turf, but the spreads are real.

5. Oracle-window arbitrage

Permissionless DEX perps (Hyperliquid HIP-3, Ostium) often update their oracle every 1-3 seconds. If the underlying spot/CME tape moves faster than the oracle refreshes, latency arbitrage windows open. Mitigation: use venues with sub-second oracles or stick to assets with deep, real-time price feeds.

NeuralArB Insight — Our internal data shows the funding-rate arbitrage strategy between Hyperliquid and Binance on equity perps yielded an average gross APR of 38% in Q1 2026, before fees, with sharply higher returns during earnings season and Fed days. See our companion piece Hyperliquid vs CEXs: Is Perp Arbitrage Still Worth It After Fees, Funding, and Slippage?

📥 Downloadable: Complete TradFi Perpetuals Exchange Matrix

A single comparison table covering the nine major venues, their max leverage, regulatory status, funding cadence, asset coverage, and KYC requirements.

Exchange / Venue | Asset Classes Offered | Max Leverage | Regulatory Status | 24/7 | Funding Freq | KYC | Key Notes |

|---|---|---|---|---|---|---|---|

Kraken (xStocks Perp) | US Equities, Indices, Gold | 20× | Yes (BMA-licensed PDSL) | ✅ | 8h | Yes (non-US) | First regulated tokenized-equity perp; SPY, NDX, NVDA, AAPL, TSLA |

Hyperliquid (HIP-3) | Commodities, Equities, FX, Indices | 50× | On-chain, non-custodial | ✅ | 1h / 8h | Wallet only | Permissionless market creation; S&P 500 licensed via Trade[XYZ] |

Binance (TradFi Perps) | Gold, Silver, Oil, FX, Indices | 50× | Offshore licensing | ✅ | 8h | Yes | 62.7% market share; dominant entrant since Jan 2026 |

BitMEX | Commodities, Equities | 100× | Seychelles-regulated | ✅ | 8h | Yes | +1,322% growth in Q1 2026; deep gold/oil liquidity |

Bitnomial | BTC/ETH perps, US equities (planned) | 10-25× | CFTC-regulated DCM (US) | ✅ | 8h | Yes (US) | First CFTC-approved perpetual futures DCM |

dYdX v4 | Crypto + select TradFi via oracles | 20× | On-chain, non-custodial | ✅ | 1h | Wallet only | Cosmos-based; growing TradFi list |

Ostium | FX, commodities, indices | 200× | On-chain (Arbitrum) | ✅ | Continuous | Wallet only | Pure RWA-focused perp DEX |

Aster | Crypto + TradFi RWAs | 100× | On-chain | ✅ | 8h | Wallet only | +131% Q1 growth; multi-chain |

CME (Traditional Future) | Equities, FX, commodities, rates | 10-20× | CFTC + clearinghouse | ❌ (RTH/ETH) | N/A — expiry-based | Yes (broker) | Industry benchmark; no funding, monthly/quarterly expiries |

Risk Map: What Every TradFi Perp Trader Must Watch

Perpetuals are not a free lunch. The four most underestimated risks in 2026:

- Oracle risk. A tokenized-equity perp is only as honest as its price feed. When the underlying stock market is closed, the oracle relies on xStock NAV, OTC quotes, or pre-market futures — all of which can be gamed during low-liquidity hours. The Kraken xStocks framework mitigates this with 1:1 collateralized SPL tokens and Chainlink Proof-of-Reserve attestations.

- Funding-rate flips. A 30% APR funding harvest can become a negative 80% APR drain if sentiment reverses mid-trade. Auto-unwind triggers are mandatory.

- Regulatory cliff risk. The CFTC’s posture is evolving but unsettled. Products offered to non-US clients today (e.g., Kraken xStocks Perp) may face geographic re-classification as US rules harden.

- Liquidity vacuums during weekends. Spreads on equity perps can blow out from 1bp to 30bp during Sunday morning Asian hours, turning a “market-neutral” trade into a stop-loss event.

The MINIMAL EDIT PRINCIPLE for risk management: don’t widen your exposure to chase exotic perps until your funding/oracle/slippage model has 90+ days of live data.

What’s Next: The 12-Month Outlook

- More indices on-chain. Expect Russell 2000, MSCI EM, FTSE 100, and Nikkei 225 perps before end of 2026, following the S&P 500 / Trade[XYZ] precedent.

- Onshore US perps. Bitnomial, Coinbase Derivatives, and CME’s own perpetual-style offering will compete for retail US flow under CFTC supervision (CFTC).

- Vertical-specific DEXs. Niche perp protocols for sports & event contracts, carbon credits, and political prediction markets will fragment liquidity but create fresh arbitrage corridors.

- AI-driven execution. Reinforcement-learning agents — like those powering NeuralArB — will dominate cross-rail arbitrage as latencies compress below human reaction time.

💬 Frequently Asked Questions (FAQ)

What is a TradFi perpetual?

A TradFi perpetual is a perpetual swap (a derivative with no expiry date) whose underlying is a traditional-finance asset — a stock, an equity index, a commodity, or an FX pair — rather than a cryptocurrency. It trades 24/7, uses funding payments to anchor to spot, and can be margined in crypto stablecoins or fiat.

How is a TradFi perp different from a CME future?

Three core differences: (1) TradFi perps never expire; CME futures have monthly/quarterly expiries. (2) TradFi perps trade 24/7 across weekends; CME products respect exchange sessions. (3) TradFi perps use a funding-rate mechanism to keep the mark tethered to spot, whereas CME futures use expiry-driven convergence. See the Wharton primer on perpetual futures pricing for the formal model.

Are TradFi perpetuals legal in the United States?

As of May 2026, most TradFi perp products are offered to non-US clients only. Kraken’s xStocks Perp explicitly excludes US customers. However, the CFTC has begun permitting BTC/ETH perpetual futures listings on US-regulated DCMs and has opened a public consultation on broader perpetual rules. Expect onshore US tokenized-equity perps within 12-24 months.

What is funding-rate arbitrage on TradFi perps?

Funding-rate arbitrage is a delta-neutral strategy where a trader takes opposing positions — long the underlying (or a perp paying negative funding) and short a perp paying positive funding. The trader collects the funding payment as a continuous yield while remaining indifferent to price direction. CoinGlass and Bitget both publish live cross-venue funding tables used by professional desks.

Which exchange has the best TradFi perps right now?

There is no single winner — it depends on your priority:

- Maximum regulation & equity coverage → Kraken xStocks Perp

- Maximum asset diversity & permissionless markets → Hyperliquid HIP-3

- Deepest commodity liquidity → Binance and BitMEX

- US onshore access → Bitnomial Refer to the downloadable matrix above for the full comparison.

What leverage can I get on a TradFi perpetual?

Leverage ranges from 5× (institutional CME-style products) up to 200× on permissionless perp DEXs like Ostium. The mainstream sweet spot for TradFi perps is 20× to 50×, which Kraken, Hyperliquid, Binance, BitMEX, and dYdX all support.

Are tokenized stocks the same thing as a stock?

No. A tokenized stock (xStock, bStock, etc.) is a blockchain token backed 1:1 by the underlying equity held in custody by a regulated issuer. You get economic exposure (price + sometimes dividends) but no voting rights, no direct shareholder relationship, and your legal claim is on the issuer, not on the company. The price tracks the equity closely but can deviate during illiquid hours — which is where arbitrage opportunities are born.

What's the biggest risk in TradFi perpetual arbitrage?

Oracle and liquidity risk during off-hours. When NYSE is closed, the price feed for a TSLAx perp leans on xStock NAV, OTC quotes, or futures references — all of which can be thin or manipulated. A “market-neutral” carry trade can blow up in a 30-minute weekend wick. Always size to survive the worst Sunday-morning print of the year.

Can AI bots really compete in this market?

Yes — and they already dominate it. Cross-rail arbitrage requires sub-second monitoring of 4+ venues, dynamic funding-rate forecasting, and capital reallocation across margin accounts. Human traders can run one leg manually; automated systems run hundreds simultaneously. Platforms like NeuralArB combine reinforcement learning with multi-venue order routing to capture spreads that disappear faster than a human can click.

How do I start trading TradFi perpetuals safely?

- Start tiny. Allocate ≤2% of trading capital while you learn the funding-rate cadence on each venue.

- Paper-trade for two weeks to map out weekend-gap and earnings-week behavior.

- Use delta-neutral structures first (funding harvest, cross-venue arbitrage) — directional perp trading at 50× leverage is the fastest way to get liquidated.

- Automate with a tested system before scaling. See our beginner guide: Crypto Arbitrage 101.

Key Takeaways

- TradFi perpetuals took 0.03% → 1.72% of crypto derivatives volume in one quarter — a structural shift, not a fad.

- Commodities (silver, oil, gold) and high-beta equities (NVDA, MSTR, TSLA) dominate flow.

- The funding-rate mechanism is the central design innovation — and the central arbitrage opportunity.

- Kraken, Hyperliquid, Binance, BitMEX, and Bitnomial are the venues to watch; CME remains the institutional benchmark.

- Cross-rail arbitrage between crypto perps and traditional futures is the highest-edge strategy in 2026 — but it requires automation, robust risk controls, and continuous monitoring of oracle, funding, and liquidity risk.

🚀 Ready to Capture the TradFi-Perp Arbitrage Edge?

Manually tracking funding rates, oracle deviations, and basis spreads across nine venues is impossible. NeuralArB’s AI-driven arbitrage engine runs cross-rail strategies across crypto and tokenized TradFi markets 24/7 — capturing dislocations the moment they appear.

✅ Multi-venue funding-rate scanner across Kraken, Hyperliquid, Binance, BitMEX, dYdX

✅ Delta-neutral execution with automated unwind triggers

✅ Reinforcement-learning agents tuned for weekend and event-driven volatility

✅ Transparent backtests & live performance dashboards

Sources & Further Reading

- BitMEX — Q1 2026 Derivatives Report: The TradFi Perpetual Swap Revolution

- Kraken — Announcing the world’s first regulated, tokenized-equity perpetual futures

- S&P Global Press — S&P 500 Licensed to Trade[XYZ] for Perpetuals on Hyperliquid

- CFTC — Staff Seek Public Comment on Perpetual Contracts

- Pillsbury Law — CFTC Permits Listing of Perpetual Futures on BTC and ETH

- Wharton Finance — Perpetual Futures Pricing (Academic Paper)

- Binance Research — The Rise of TradFi-Perps Weekly

- a16z via Moomoo — Perpetual Contracts Are Rewriting Global Trading Rules

- CoinDesk — Hyperliquid HIP-3 Hits $1.2B Open Interest

Disclaimer: These materials are for general information purposes only and are not investment advice or a recommendation or solicitation to buy, sell or hold any cryptoasset or to engage in any specific trading strategy. Some crypto products and markets are unregulated, and you may not be protected by government compensation and/or regulatory protection schemes. The unpredictable nature of the cryptoasset markets can lead to loss of funds. Tax may be payable on any return and/or on any increase in the value of your cryptoassets and you should seek independent advice on your taxation position.