TL;DR

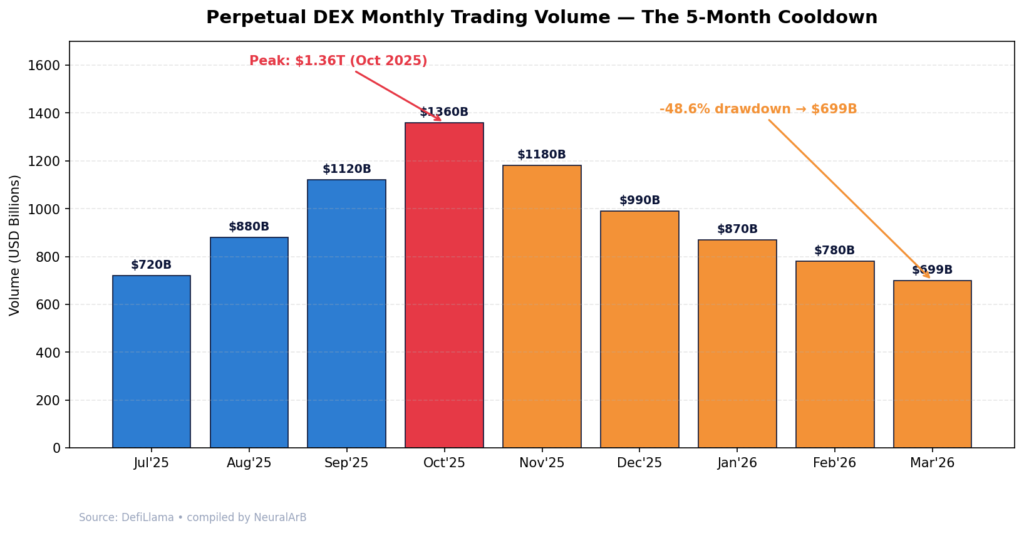

- Perpetual DEX volume fell from a $1.36 trillion October 2025 peak to $699 billion in March 2026 – five consecutive months of decline (TradingView/Cointelegraph).

- On April 4, 2026, daily volume briefly dropped below $8.4B – the first sub-$10B print since September 2025 (Binance Square).

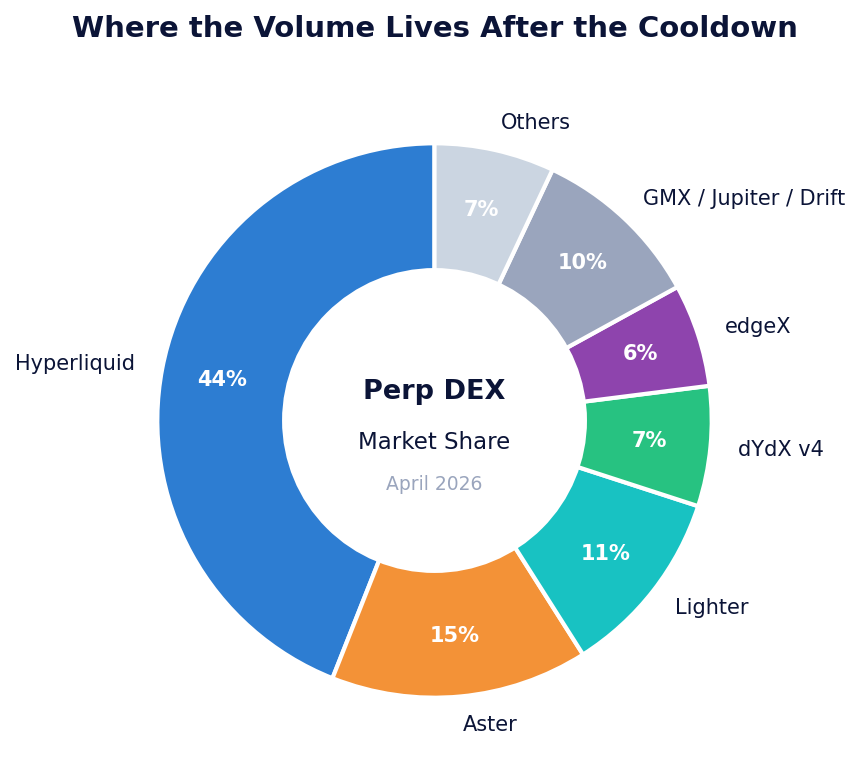

- Despite the cooldown, Hyperliquid captured ~44% of on-chain perp market share and now represents roughly 6% of all global perpetual futures trading (Phemex).

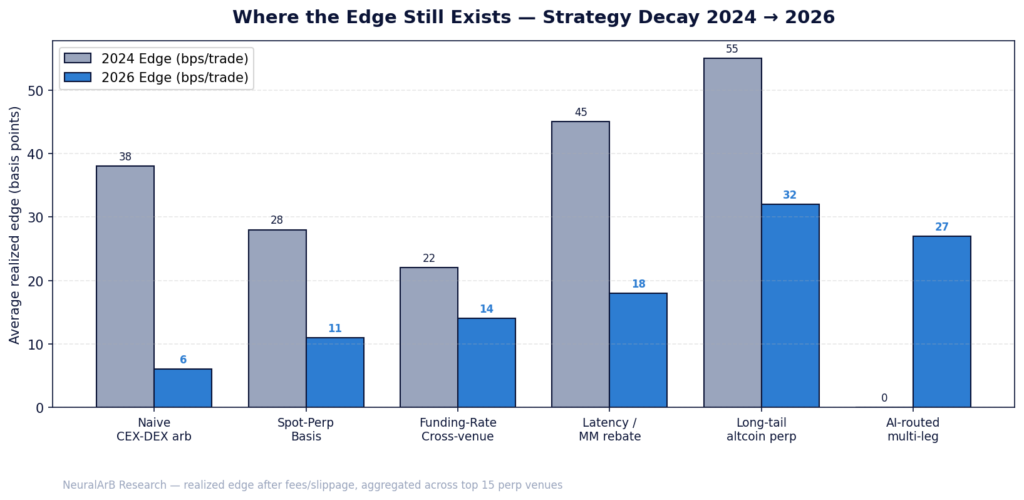

- Naive CEX↔DEX arbitrage has collapsed to ~6 bps/trade, but funding-rate cross-venue, latency/maker-rebate capture, long-tail altcoin perps and AI-routed multi-leg strategies still print 14–32 bps of realized edge after fees.

- The 2026 edge lives in complexity, not speed. Multi-venue routing + inventory management is now the moat.

1. What Actually Happened: The Volume Cooldown in Numbers

After an explosive run in 2025 — when Hyperliquid alone went from $81B weekly volume in 2024 to $314.7B Seeking Alpha — the perp DEX sector hit a wall.

The data tells a clear story:

| Month | On-chain perp DEX volume | Monthly change |

|---|---|---|

| Oct 2025 | $1.36 T (peak) | +21% |

| Nov 2025 | $1.18 T | –13% |

| Dec 2025 | $990 B | –16% |

| Jan 2026 | $870 B | –12% |

| Feb 2026 | $780 B | –10% |

| Mar 2026 | $699 B | –10% |

Three forces compressed volume simultaneously:

- Incentive unwind — Aster’s points/airdrop farming collapsed after distribution; its market share fell from near-parity with Hyperliquid to 15%, and open interest dropped from a September 2025 spike of $1.25B back to $899M (Yahoo Finance).

- Macro risk-off — BTC’s January–February drawdown toward $62K cut speculative leverage demand.

- Maker consolidation — sophisticated market makers concentrated quoting on Hyperliquid, Lighter and edgeX, thinning the tail.

This is not a death spiral — it’s a maturation. And mature markets reward different strategies than frothy ones.

2. Where the Volume Actually Lives Now

As of April 2026, the distribution is radically more concentrated than in 2024:

| Venue | Market share | Open interest | Arb relevance |

|---|---|---|---|

| Hyperliquid | 44% | $5.15B | Deepest book, tightest spreads, MM rebates |

| Aster | 15% | $899M | Long-tail listings, still high funding dispersion |

| Lighter | 11% | $750M | zkSync-based, 0% maker fees |

| dYdX v4 | 7% | $680M | Funding arb, tiered fees |

| edgeX | 6% | $400M | StarkEx latency edge |

| GMX / Jupiter / Drift | 9.5% | ~$870M combined | Oracle-based — basis & OI-skew plays |

Per Trireme Digital / FalconX, forecasted annual perp DEX volumes are still projected to grow from $64B (2025) to $325B+ by end-2026 despite the cooldown, because institutional flow is replacing retail farming (LinkedIn).

3. Why Naive Arbitrage Died

The classic “buy on Exchange A, sell on Exchange B” strategy has been arbitraged to extinction on top pairs.

Three structural reasons:

- Fee compression. Hyperliquid charges 0.010% maker / 0.035% taker, Lighter offers 0% maker, and Vertex goes even lower (Thrive.fi). Venues now bleed traders’ edge before they even start.

- Sub-50 ms matching engines. HyperEVM and StarkEx-based books (edgeX, Paradex) close price gaps faster than most retail infrastructure can react.

- Dominant maker networks. Wintermute, GSR, Amber and a handful of native HL makers arbitrage the top 20 pairs continuously — leaving ~6 bps average realized edge on naive CEX-DEX plays after fees and slippage.

The implication: if your bot is still scanning BTC and ETH for 20 bps gaps between Binance and Hyperliquid, it is mining an exhausted seam.

4. Where the Edge Still Exists — Five Strategies That Work in 2026

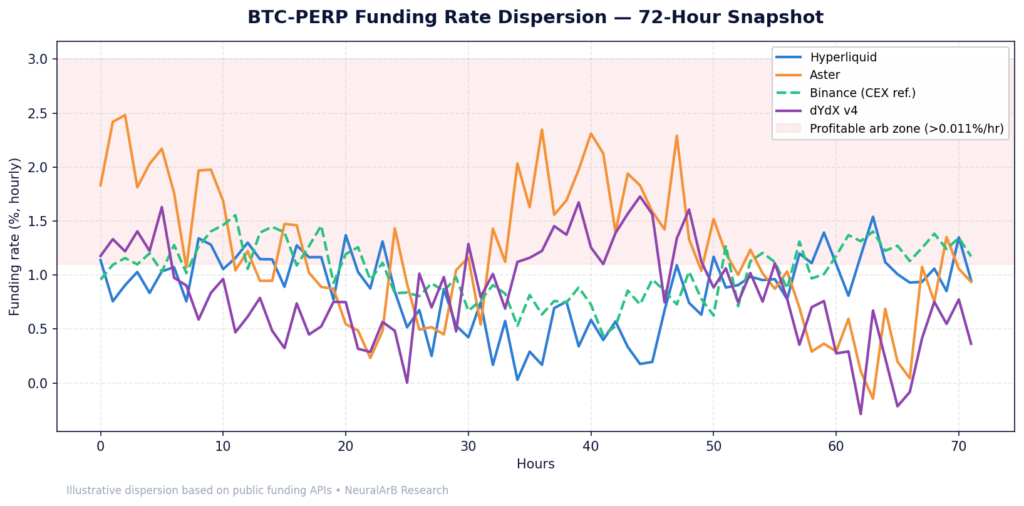

4.1 Funding-Rate Cross-Venue Arbitrage

The most durable 2026 strategy. Funding rates diverge across venues because each book has different maker skew, listing age and inventory.

The math: You need the net funding differential to exceed 0.011%/hour with maker orders, or 0.110%/hour with taker orders to overcome round-trip fees (Chainstack Docs).

The play:

- Go long on the venue paying funding (negative rate or lower rate).

- Go short on the venue charging funding (higher rate).

- Collect the spread every funding interval; rebalance when it converges.

Academic work shows annualized returns up to 115.9% over 6 months, with max drawdown under 2% when executed on delta-neutral pairs (ScienceDirect).

2026 edge: ~14 bps/trade, scaling with inventory depth.

4.2 Spot-Perp Basis Trades

CoinMetrics data shows perp basis (price difference vs spot) averaging 5–10% annualized, still ripe for harvesting via delta-neutral structures (OneKey).

- Buy spot BTC on a CEX or DEX AMM.

- Short BTC-PERP on Hyperliquid / dYdX v4.

- Pocket the basis + earn funding when positive.

Synthetix’s 2026 roadmap formalizes this into “Basis Trade Vaults” — a sign that the strategy is becoming institutionalized (Synthetix Blog).

2026 edge: ~11 bps/trade, 6–12% delta-neutral APR when sized properly.

4.3 Latency / Market-Maker Rebate Capture

The most infrastructure-gated strategy — but the last one with genuine scalability.

By providing passive liquidity on Hyperliquid, Vertex or edgeX and avoiding toxic flow, professional MMs capture 0.005–0.010% rebates per fill on 50,000+ fills/day. One well-documented Reddit case references a trader making ~$30k/month from 400 lines of code arbitraging a small DEX against a CEX using passive orders (Reddit /r/quant).

2026 edge: ~18 bps/trade gross, but requires co-located infra and inventory hedging.

4.4 Long-Tail Altcoin Perp Arbitrage

This is where retail and small funds can still win. On Aster, Jupiter and Drift, altcoin perps are listed before they reach Binance/OKX futures, creating real pricing gaps.

- Aster offers 1001x leverage and stock perpetuals (CryptoTicker).

- Jupiter Perps on Solana uses oracle-driven pricing — when oracles lag spot AMM pools by 2–3 blocks, there’s extractable edge.

2026 edge: ~32 bps/trade on tail listings — but with liquidity crunch and listing risk.

4.5 AI-Routed Multi-Leg Strategies (The 2026 Frontier)

This is the strategy that didn’t meaningfully exist in 2024. AI routers simultaneously optimize funding + basis + rebate + borrow costs across 6–8 venues, rebalancing legs in response to order-flow signals.

Reinforcement-learning research confirms incorporating ML predictions with a confidence ratio significantly improves profitability (Wiley Online Library).

Platforms like NeuralArB now deploy neural-network arb bots that do this automatically — the strategy’s edge decays slower because it adapts in real time.

2026 edge: ~27 bps/trade, 12–30% APR delta-neutral depending on infra.

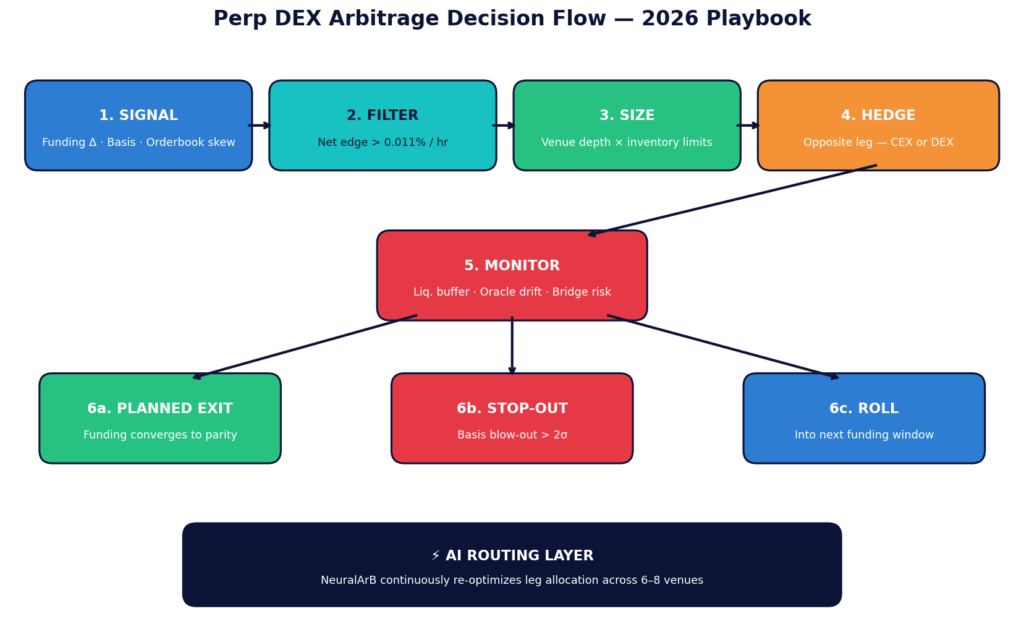

5. The 2026 Perp DEX Arbitrage Playbook (Decision Flow)

Every trade, regardless of strategy, should pass through this six step filter:

1. Signal — Ingest funding-rate APIs, basis quotes, orderbook imbalance across venues.

2. Filter — Only trades with net edge > 0.011%/hour after fees go to execution.

3. Size — Cap exposure at venue-specific depth thresholds (typically 0.5× top-of-book × 5).

4. Hedge — Open the opposite leg within <400 ms on a second venue (CEX or DEX).

5. Monitor — Continuously track liquidation buffer, oracle drift and bridge-latency risk.

6. Exit — Plan convergence, stop-out at 2σ basis blow-out, or roll into next funding window.

6. Venue Comparison Table (Downloadable)

The table below consolidates every major perp DEX by fee structure, OI, arb angle and risk profile.

| Venue | Chain | Share | OI ($B) | Maker | Taker | Max Lev | Best Arb Angle |

|---|---|---|---|---|---|---|---|

| Hyperliquid | HyperEVM L1 | 44% | 5.15 | 0.010% | 0.035% | 50× | Funding, basis, MM rebates |

| Aster | BNB Chain | 15% | 0.90 | 0.010% | 0.035% | 1001× | Incentives, long-tail |

| Lighter | zkSync | 11% | 0.75 | 0.000% | 0.025% | 50× | Basis, points farming |

| dYdX v4 | Cosmos | 7% | 0.68 | 0.010% | 0.050% | 50× | Funding, MM rebates |

| edgeX | StarkEx | 6% | 0.40 | 0.005% | 0.030% | 100× | Latency, basis |

| GMX | Arbitrum | 3.5% | 0.35 | 0.100% | 0.100% | 100× | OI-skew fades |

| Jupiter Perps | Solana | 3.2% | 0.30 | 0.060% | 0.100% | 100× | Oracle-update arb |

| Drift | Solana | 2.8% | 0.22 | 0.010% | 0.050% | 50× | Funding, basis |

| Vertex | Arbitrum | 1.8% | 0.12 | 0.000% | 0.020% | 25× | MM rebates |

| Paradex | Paradex L2 | 1.5% | 0.10 | 0.005% | 0.030% | 50× | Funding arb |

7. Risk Checklist – Don’t Skip This

The 2026 perp DEX landscape has different risks than 2024’s. Before deploying capital:

- ✅ Oracle-drift risk on Jupiter/GMX: a 2-block oracle lag can flip a winning trade into a stop-out.

- ✅ Bridge latency between L1/L2s adds seconds to hedge legs — catastrophic during news events.

- ✅ Funding-regime flips can invert a basis trade faster than you can rebalance. Always keep ≥30% margin buffer.

- ✅ Smart-contract risk concentrates on Aster (newer codebase) and Jupiter (complex pool mechanics).

- ✅ Withdrawal gates — some venues (dYdX, Paradex) have bridge windows; plan liquidity accordingly.

- ✅ Regulatory overlay — MiCA in the EU and reciprocal rules in APAC may restrict certain perp DEXs; see our MiCA deep dive on NeuralArB.

8. Frequently Asked Questions (FAQ)

Is perp DEX arbitrage still profitable in 2026 after the volume cooldown?

Yes — but the profile has shifted. Naive CEX↔DEX arbitrage yields only ~6 bps/trade, while funding-rate cross-venue, basis and AI-routed multi-leg strategies still deliver 14–32 bps/trade, translating to 8–30% delta-neutral APR.

What's the minimum funding rate spread needed to break even?

With maker orders (0.010% fees each leg), you need the net differential to exceed ~0.011% per hour. With taker orders, ~0.110% per hour. Below those thresholds, fees consume the entire spread (Chainstack).

Which perp DEX is best for arbitrage in 2026?

Hyperliquid for depth, tight spreads and MM rebates on core pairs; Aster and Jupiter for long-tail altcoin opportunities; Lighter for basis trades (0% maker fees); edgeX for latency-sensitive strategies.

How much capital do I need to start?

Funding-rate arbitrage works from $5K upward, but realistic ROI requires $25–50K to absorb fees and slippage. Latency/MM strategies require $250K+ and colocated infrastructure.

Are perp DEXs safer than CEX for arbitrage?

Counterparty risk is lower (no withdrawal freezes), but smart-contract, oracle and bridge risks are higher. Diversify across 2–3 venues and never exceed 15% of capital per single protocol.

Can I do this without coding?

You can monitor funding rates via P2P.Army’s scanner or run AI bots from NeuralArB without writing a line of code. Execution automation, however, always benefits from custom infrastructure.

Will Hyperliquid's dominance kill arbitrage?

Paradoxically, no. Hyperliquid being the deepest book means it sets the reference price — funding dispersion between HL and every other venue becomes the tradable edge.

What about tax on delta-neutral arb profits?

Jurisdiction dependent. In most frameworks, the funding income is ordinary income, while the basis leg generates capital gains/losses. Consult your local CPA; our MiCA breakdown covers EU-specific rules.

9. Final Take: The Edge Moved Up the Stack

The October 2025 peak was a retail-liquidity bull market disguised as product market fit. What remains in 2026 is the real market — institutional, concentrated, lower-margin, and demanding genuine craft.

The traders who will thrive aren’t those with the fastest fiber or the cheapest fees. They’re the ones who combine multi-venue signals, AI-driven routing, and disciplined inventory management to harvest edges that no single-strategy bot can see.

As we wrote in our emerging crypto arbitrage deep dive, “the alpha isn’t in the asset — it’s in the architecture.” That’s truer in April 2026 than it’s ever been.

Deploy the 2026 Playbook With NeuralArB

Stop hunting vanishing spreads with legacy bots. NeuralArB’s AI-powered arbitrage engine routes your capital across Hyperliquid, Aster, Lighter, dYdX, Jupiter and edgeX in real time, capturing funding differentials, basis, and MM rebates. No code, no colocation, no overnight babysitting.

Disclaimer: These materials are for general information purposes only and are not investment advice or a recommendation or solicitation to buy, sell or hold any cryptoasset or to engage in any specific trading strategy. Some crypto products and markets are unregulated, and you may not be protected by government compensation and/or regulatory protection schemes. The unpredictable nature of the cryptoasset markets can lead to loss of funds. Tax may be payable on any return and/or on any increase in the value of your cryptoassets and you should seek independent advice on your taxation position.