Executive Summary: The Tokenized Stock Revolution Happened (And It’s on Solana)

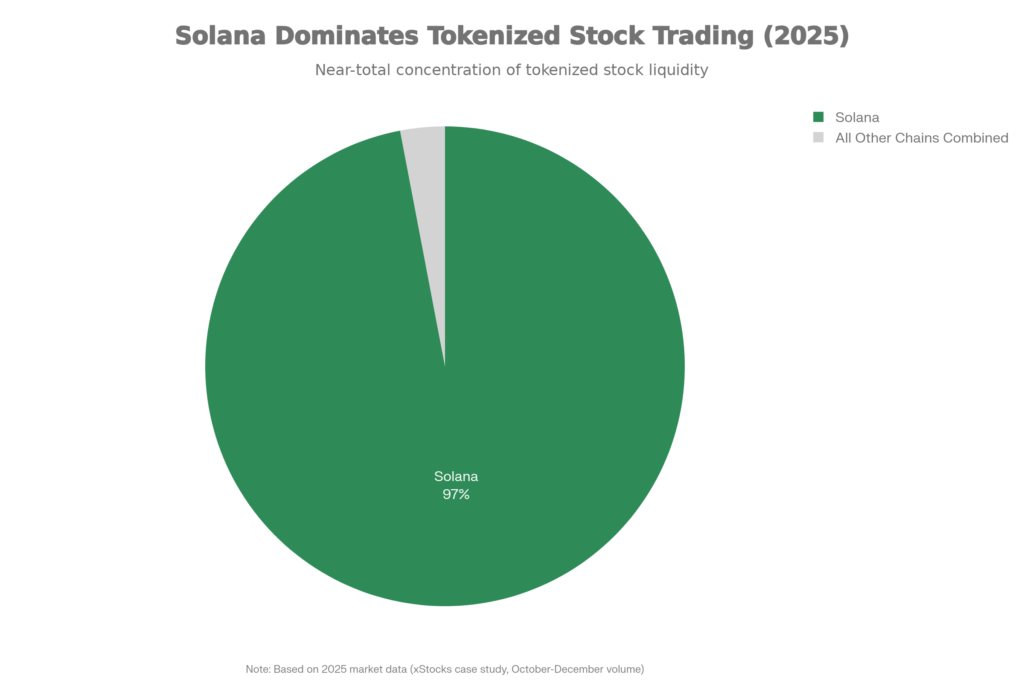

While most of the crypto industry debated whether real-world assets (RWAs) would ever achieve meaningful scale, tokenized stocks quietly exploded on Solana in 2025, capturing $2.1B+ in volume in just six weeks and commanding 95-99% of all tokenized equity trading globally.

For high-frequency traders, this concentration presents an extraordinary arbitrage frontier:

24/7 trading of blue-chip equities (AAPL, TSLA, NVDA, GOOGL) when traditional markets are closed

Sub-millisecond latency and near-zero fees ($0.00025/transaction) on Solana vs. $5-50 on older blockchains

Multi-venue price discovery across CeFi exchanges (Bybit, Kraken) and Solana DeFi protocols simultaneously

Regulatory legitimacy through Swiss and EU custodial oversight, not gray-market experimentation

Compound strategies combining spot arbitrage, lending protocols, and synthetic perpetuals

Unlike previous RWA hype cycles, this isn’t theoretical—it’s operational, liquid, and structurally rich for arbitrage.

The problem: Most traders know tokenized stocks exist. Almost none have the infrastructure to capture the edge.

This guide covers what you need to know: how the arbitrage actually works, where the spreads appear, why Solana’s infrastructure is irreplaceable for this strategy, and what it takes to compete at high frequency.

Part 1: What Are Solana Tokenized Stocks and Why They Matter

Definition and Mechanics

Solana tokenized stocks are SPL tokens (Solana’s native token standard) that represent 1:1 claims on real equities held in regulated custodial vaults, typically under Swiss (SIX) or EU oversight. A token labeled “xAAPL” or “AAPL-SOL” doesn’t create synthetic exposure—it’s backed by actual Apple shares sitting in a bank custody account, transferable via blockchain for settlement speed but redeemable for the underlying equity.

Key platforms (as of late 2025):

xStocks: First mover, now dominant venue with $2.1B+ cumulative volume

Bonk Finance/other DEX native options: Smaller but growing venues

Multiple CeFi venues (Bybit, Kraken, Upbit) offering spot trading in tokenized equities

This structure is fundamentally different from crypto synthetics (which are just collateralized debt positions) and different from derivatives (which create leverage or leverage-free hedging). A tokenized AAPL share IS a real share, just on-chain and composable.

Why Now? Why Solana?

Timing Confluence:

Regulatory clarity (2024-2025): Swiss Financial Market Supervisory Authority (FINMA) and EU regulators provided frameworks for tokenized securities custody

Institutional demand: Traditional finance started seeking 24/7 trading and programmable settlement

Solana’s infrastructure maturity: After 2023-2024 stability improvements, Solana could reliably support this use case

DeFi composability: Ability to use tokenized stocks as collateral, in LPs, and in complex instruments created network effects

Why Solana specifically (vs. Ethereum, Avalanche, etc.):

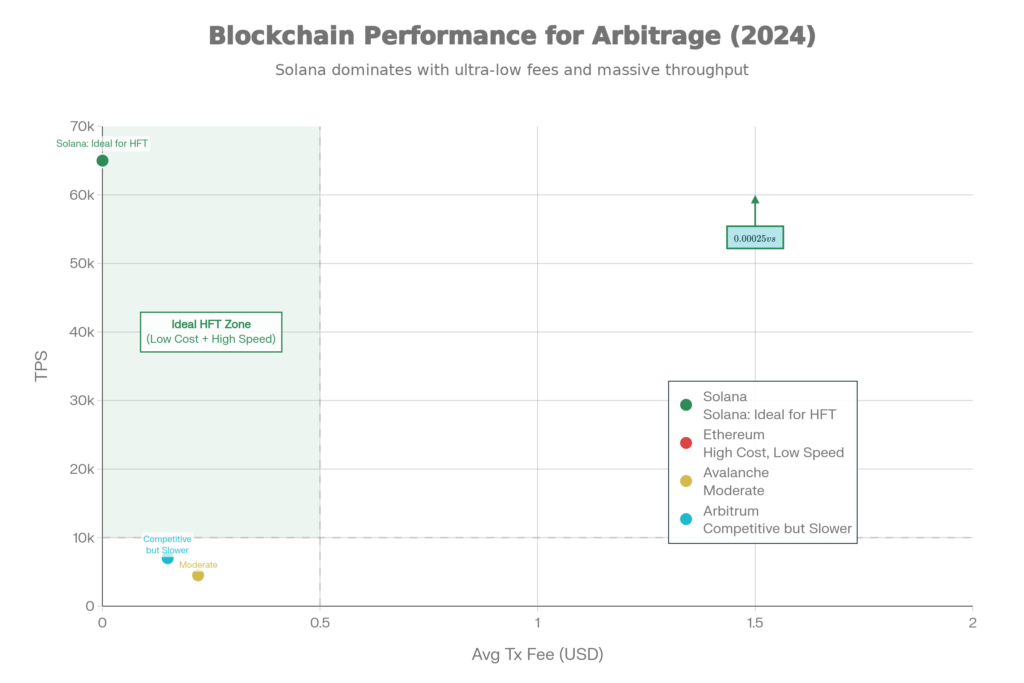

Solana’s combination of speed (sub-second blocks), cost ($0.00025/tx), and finality (confirmed in ~400ms) is uniquely suited to frequent trading of fractional positions. Ethereum’s $5-50 per transaction cost makes arbitraging 0.2% spreads economically nonsensical. Avalanche and other L1s are faster than Ethereum but still 100x slower and 1000x more expensive than Solana.

For an arbitrage bot executing 100+ trades daily, Solana fees are negligible; Ethereum fees are a dealbreaker.

Part 2: The Arbitrage Landscape

Three Main Arbitrage Circuits

1. CeFi-DeFi Arbitrage (The Core Trade)

The simplest arbitrage loop: capture spreads between centralized exchanges and Solana DEXs.

Real example (December 2025 snapshot):

Tokenized AAPL on Bybit: $197.50 (fair value)

AAPL_xSPL on Raydium (Solana AMM): $201.20 (1.87% premium)

Spread opportunity: 1.87%

Bot execution:

1. Sell 100 AAPL_xSPL on Raydium at $201.20 → Receive $20,120 in USDC

2. Bridge USDC to Bybit

3. Buy 100 AAPL tokens on Bybit at $197.50 → Spend $19,750

4. Gross profit: $370 (1.87%)

5. Minus: Slippage ($50), gas/fees ($10), bridge fee ($20), slippage on buy ($40)

6. Net profit: $250 per 100 shares = 1.27% net

DeFi venues can trade at premiums when:

Staking or yield farming rewards make holding the token attractive

Liquidity is thin and large buys move price up

On weekends/after-hours when CeFi liquidity dries up relative to Solana

This spread isn’t free money—it’s capital trapped in the difference between when-available markets. But on Solana’s timescale, bots can arbitrage these differences dozens or hundreds of times daily.

2. DEX-DEX Arbitrage (Intra-Solana)

Even within Solana, multiple DEXs and liquidity pools create inefficiencies.

Raydium AAPL-USDC pool

Orca AAPL-USDC pool

Phoenix DEX AAPL order book

Smaller venues (Dexlab, etc.)

When a large order hits one venue, others may not adjust price instantly. Arbitrage bots:

Buy from the lagging venue

Immediately sell to the price-leader venue

Capture the micro-spread

These edges are smaller (0.05-0.2%) and require fast execution (sub-second), but with zero-cost settlement on Solana, they’re viable at scale.

3. Basis and Carry Trades (Advanced)

Using Solana’s lending markets (Solend, Marinade, others), bots can:

Lend out tokenized AAPL at 2-4% APY (collateral rates for equity tokens)

Simultaneously short AAPL-USDC perpetuals at +0.05% funding

Capture the difference (2-4% minus funding minus basis risk)

This is capital-intensive (requires AAPL shares to lend) but low-risk when executed with proper hedging.

Part 3: Why Solana Infrastructure Is Non-Negotiable

Latency and Throughput Requirements

High-frequency arbitrage depends on speed. Consider:

At Ethereum’s 12-second block time and $5-50 per transaction, a spread that closes in 4 seconds means:

You either miss the edge entirely (bot isn’t fast enough)

Or you pay so much in fees that the edge evaporates

At Solana’s ~400ms average latency and $0.00025 per transaction:

You have time to observe the spread, compute the route, and execute before it closes

Fees are negligible even for small edges

Concrete performance comparison:

| Metric | Solana | Ethereum | Arbitrum |

|---|---|---|---|

| Block Time | ~400ms | ~12s | ~250ms (L2) |

| TX Fee | $0.00025 | $5-50 | $0.15 |

| Fee as % of 0.5% Spread | 0.00005% | ~0.5-5% | ~0.03% |

| Trades/Day Feasible | 100-500+ | <5 | 20-50 |

On Solana, a bot executing 200 trades daily at $0.00025/trade costs $0.05 total in fees—negligible. On Ethereum, the same strategy costs $1,000-10,000 in fees, making it uneconomical unless spreads are 1%+ (extremely rare).

Parallel Execution and Order Flow

Solana’s block engine allows multiple transactions from different users (and bots) to be processed in parallel within a single block, as long as they touch different state accounts. This means:

Your arbitrage order won’t necessarily interfere with other bots’ orders in the same block

The network can handle hundreds or thousands of arbitrage attempts simultaneously

Price discovery becomes more efficient

Older blockchains serialize transactions more strictly, creating bottlenecks during high-volume periods.

Part 4: Risk and Limitations

Execution Risks

Even on Solana, arbitrage carries risks:

Slippage: Pools might be shallower than expected, turning a theoretical 1% edge into a loss.

MEV/Sandwich Attacks: If your transaction is visible in the mempool, adversarial bots can front-run you. Professional setups use private transaction pools or encrypted ordering to mitigate this.

Bridge/Route Risk: Moving capital between CeFi and Solana adds:

Time lag (minutes, not milliseconds)

Counterparty risk (exchange custody of your tokenized stock)

Transfer fees

Regulatory and Custody Risk

Tokenized stocks aren’t unregulated crypto. They’re regulated securities backed by custodians subject to financial oversight. This creates:

Counterparty Risk: If xStocks’ custodian fails, you hold claims on shares locked in bankruptcy.

Regulatory Risk: Authorities could restrict who can trade tokenized stocks in which jurisdictions, freezing some accounts or venues.

Compliance Risk: Transfers may be subject to programmatic compliance rules (restrictions on transfer to certain addresses, mandatory pause during corporate actions like dividends).

These risks are manageable but require due diligence. A bot that assumes tokens can be freely transferred 24/7 might fail on dividend day when transfers are paused.

Liquidity and Spread Volatility

The tokenized stock market is still nascent. Liquidity is concentrated:

Tier 1 names: AAPL, TSLA, NVDA, GOOGL—liquid across multiple venues, spreads 0.05-0.5%

Mid-tier names: Ford, Intel, AMD—liquid on Solana DEXs, less on CeFi, spreads 0.3-1%

Niche names: Micro-cap or less liquid stocks—thin order books, spreads 1-5%, low volume

A naive bot that treats all tokenized stocks equally will lose money on low-liquidity names where slippage exceeds theoretical edge.

Part 5: Building a Real High-Frequency Strategy

Core Components

A production HFT setup for Solana tokenized stocks requires:

1. Data Infrastructure

Real-time websocket feeds from multiple DEXs (Raydium, Orca, Phoenix)

Pyth/Switchboard oracle feeds for reference pricing

CeFi exchange APIs (Bybit, Kraken) for spot prices

Latency-optimized aggregation (combine all feeds into unified state every 50-100ms)

2. Pricing Engine

Calculate theoretical fair value for each tokenized stock

Compute implied spreads across venues

Filter out spreads that can’t be captured after fees/slippage

3. Execution Layer

Smart order routing (split orders across venues to minimize slippage)

Risk controls (position limits, max notional per symbol, max daily loss)

Execution monitoring (track realized vs. theoretical PnL)

4. Risk Management

Portfolio-level correlation analysis (tokenized AAPL and TSLA may move together during tech sell-offs)

Dynamic position sizing (larger positions on high-liquidity names, smaller on thin books)

Stop-loss and daily P&L limits

Expected Edge Sizes and Frequencies

Realistic expectations (not marketing):

Liquid names (AAPL, TSLA): 0.05-0.3% per round-trip, 10-50 opportunities daily

Mid-tier names: 0.2-0.8% per round-trip, 3-15 opportunities daily

Thin names: 1-5% theoretical, but often uneconomical after slippage

On $500K capital, a modest HFT operation might:

Execute 50-150 round-trip trades daily

Average 0.15% net per round-trip

Capture ~0.075% daily return (~$375/day on $500K)

Annualize to ~27% (before costs, taxes, drawdowns)

These are conservative estimates. Top-tier operations with superior data and execution might achieve 2-3x these returns; naive setups often lose money.

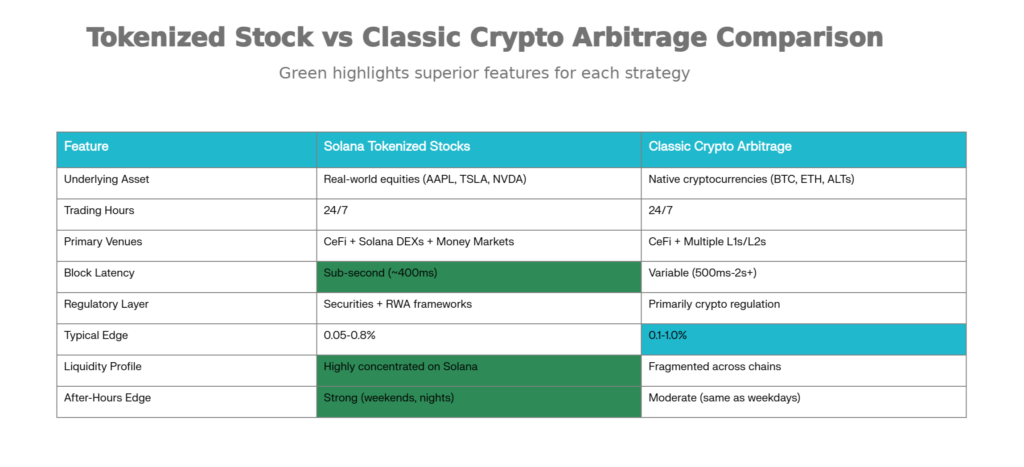

Part 6: Comparison to Classic Crypto Arbitrage

Solana tokenized stocks are not a replacement for BTC/ETH arbitrage, but a complement. They offer:

| Advantage | Impact |

|---|---|

| Real-world asset backing | Lower systemic/counterparty risk, attractive to institutions |

| 24/7 trading of equities | Capture after-hours/weekend spreads absent in traditional markets |

| Composability with DeFi | Use tokenized stocks as collateral, in LPs, in structured products—creates complex arbitrage |

| Tighter spreads | Lower volatility → smaller edges, but more consistent execution |

But they also entail:

| Disadvantage | Impact |

|---|---|

| Regulatory overhead | Jurisdictional restrictions, compliance costs |

| Custody/counterparty risk | Custodian or issuer failure could freeze your capital |

| Lower volatility | Tokenized AAPL moves with real AAPL (24/7 Solana price reflects off-chain moves), unlike crypto tokens that can spike on narrative |

| Smaller spreads | Must execute at higher frequency to achieve same absolute returns |

In practice, professional arbitrageurs likely exploit both crypto and tokenized stocks, allocating capital to whichever market offers the best risk-adjusted edges at any moment.

Part 7: The Emerging Landscape and Opportunities

Market Structure Evolution

As of December 2025:

Solana’s share: ~95-99% of global tokenized stock volume (still growing)

Total volume: $2.1B+ in six weeks on xStocks; additional volume on CeFi venues (Bybit, Kraken reported ~$500M in first week)

Tokenized names: ~15-20 liquid names (AAPL, TSLA, NVDA, GOOGL, MSFT, etc.); 50+ additional names available but with lower liquidity

Trajectory:

If adoption accelerates, tokenized stocks could represent a significant portion of Solana’s total DEX volume within 12-24 months

Institutional adoption (traditional asset managers hedging via tokenized stocks, custody providers offering tokenized wrappers) could drive 10-100x volume growth

New opportunities:

Index/basket arbitrage: Create synthetic indices (e.g., NASDAQ-100 via tokenized stocks) and arbitrage against real indices

Options-style strategies: Combine tokenized stocks with synthetic perpetuals to replicate option payoffs

Corporate action plays: Tokenized stock markets may respond to earnings, dividends, stock splits with faster repricing than CeFi, creating exploitable inefficiencies

Institutional Participation

Traditional finance is cautiously entering. Early signs:

As institutional capital enters, liquidity will deepen and spreads will tighten—but new inefficiencies may emerge at the intersection of traditional and tokenized markets.

Part 8: The Infrastructure Challenge

Why DIY Doesn’t Scale

Building a production arbitrage engine from scratch is expensive:

Data infrastructure: $50K-200K/month for co-located servers, feed aggregation, API management

Engineering: $200K-500K/year for a team that can maintain low-latency systems

Risk systems: $100K+ to build robust position tracking and correlation analysis

Compliance: $50K+ annually for legal review and regulatory monitoring

For most individual traders and small teams, this is prohibitive.

Where NeuralArB Enters (Organic Integration)

As Solana tokenized stocks have emerged as a major opportunity, the challenge for traders isn’t spotting the opportunity—it’s capturing it reliably and at scale. NeuralArB is built exactly for this environment.

NeuralArB’s infrastructure—designed for sub-second latency, multi-venue scanning, and adaptive risk management—is equally capable of arbitraging tokenized stocks on Solana as it is crypto pairs. In fact, the transition from BTC/ETH arbitrage to AAPL/TSLA arbitrage is relatively straightforward once you have:

Real-time feeds from Solana DEXs and CeFi venues (built)

Smart order routing that minimizes slippage (built)

Risk controls adapted for different asset classes (built)

24/7 execution with minimal supervision (built)

For traders already profitable on crypto arbitrage, extending into tokenized stocks adds:

New venue for capital deployment (Solana DEXs + CeFi)

New asset class uncorrelated with crypto narratives (real equity exposure)

24/7 access to equities without traditional market hours friction

The question isn’t whether tokenized stock arbitrage is profitable—market data shows it is. The question is whether you have the infrastructure to capture that profitability without building everything yourself.

For teams exploring Solana tokenized-stock arbitrage, integrating NeuralArB’s AI-driven execution layer accelerates time-to-profit significantly. Rather than spending 6-12 months engineering a low-latency system, you can deploy tested infrastructure in weeks and focus on strategy optimization and capital scaling.

Part 9: Getting Started (Practical Next Steps)

For Existing Crypto Arbitrage Traders

If you already trade BTC/ETH arbitrage profitably:

Research: Understand the xStocks ecosystem, key venues (Raydium, Orca, Bybit), and reference pricing sources

Start small: Allocate 5-10% of capital to tokenized stock pairs (AAPL, TSLA)

Monitor: Track spreads and your execution quality for 2-4 weeks before scaling

Optimize: Adjust position sizing, symbol selection, and risk limits based on live performance

Most traders find that tokenized stocks follow similar patterns to crypto pairs—spreads cluster around key times, liquidity has daily/weekly cycles, and correlation regimes shift—so the skill transfer is significant.

For New Entrants

If you’re new to arbitrage but interested in tokenized stocks:

Learn the basics: Read whitepapers on xStocks and Solana DEXs; understand custody, trading mechanics, and risk

Paper trade: Use backtesting or paper trading to develop intuition before risking capital

Start with infrastructure: Rather than building custom software, use a platform like NeuralArB that handles execution and risk—you focus on capital management

Scale gradually: Begin with $10-50K capital, grow based on realized returns and risk management discipline

Conclusion: The New Frontier Is Real

Solana tokenized stocks represent the first viable, liquid market for around-the-clock arbitrage of real-world equities. Solana’s dominance (95-99% market share) concentrates liquidity and price discovery in one place, making it uniquely suited for high-frequency trading at scales that would be uneconomical on other blockchains.

The arbitrage opportunities are real:

CeFi-DeFi spreads of 0.5-2% are consistently observable

Intra-Solana DEX inefficiencies provide daily opportunities

Advanced strategies (basis trades, basket arbitrage, corporate action plays) are emerging

But capturing these opportunities requires:

Real-time multi-venue data aggregation

Sub-millisecond execution capability

Robust risk management adapted for both crypto and equity market conditions

24/7 operational discipline

This is the definition of a frontier: opportunity exists, but so does complexity. Traders with superior infrastructure will capture disproportionate returns; those with outdated tools will underperform despite having access to the same markets.

For teams ready to move beyond theoretical interest and build real alpha in tokenized stocks, the window is open—but it’s unlikely to stay this wide forever. As more sophisticated capital enters, spreads will compress and only the best-execution engines will survive.

💬 Frequently Asked Questions (FAQ)

Is tokenized stock arbitrage "risk-free"?

No. You face execution risk (slippage may exceed theoretical edge), custody risk (if the custodian fails), regulatory risk (jurisdiction/compliance changes), and market risk (price moves against you during execution). “Arbitrage” means low-risk, not no-risk.

What's the minimum capital to start?

Theoretically $1K, but practically $50K+. Below $50K, fees and slippage likely exceed theoretical edge. At $50K with a 0.15% daily return, you’re capturing ~$75/day (~$1,875/month), which might justify the risk but doesn’t cover engineering costs if you build solo.

Can I do this manually (without a bot)?

Not profitably at scale. Spreads close in milliseconds; by the time you read them and execute manually, they’re gone. You need automated execution.

Is Solana tokenized stock trading available everywhere?

No. Geographic restrictions apply. Some venues geo-fence (e.g., US traders may be excluded). Check venue terms before building a strategy.

What happens if a token is delisted?

Depends on the platform. Typically you’d have a redemption window to swap back to underlying shares or exit on secondary markets. But this isn’t guaranteed; review platform docs.

Stay Connected:

Stay Connected:

Related Analysis:

Related Analysis:

How High-Frequency Trading (HFT) (Impacts Crypto Arbitrage)

- Reinforcement Learning in Dynamic Markets (AI trading strategies)

- Crypto Arbitrage 101 (beginner’s guide to arbitrage)

Data Sources:

- CoinGecko – Real-time price data and market cap

- Yahoo Finance – Historical price data

- CoinDesk – Liquidation data

- Reuters – Market analysis

- Binance – Upcoming catalysts

Disclaimer: This analysis is for educational purposes. Arbitrage trading involves substantial risk, including custody risk, regulatory risk, and execution risk. Past performance is not indicative of future results. Never risk capital you cannot afford to lose. Consult qualified financial and legal advisors before trading.