TL;DR

Cross-chain intent arbitrage is the next evolution of crypto execution. Instead of manually bridging assets, users or apps submit intents such as “get USDC on Base” or “swap ETH on Arbitrum for USDC on Base,” and a competitive network of solvers determines the best route and settlement path. That gives professional desks new edge through faster fills, auction-based order competition, inventory netting, and more capital-efficient settlement design. Standards like ERC-7683 make this market more interoperable, while systems like Across, UniswapX, and emerging solver infrastructure show how cross-chain execution is becoming a balance-sheet and systems game, not just a spread-detection game. [Ethereum Improvement Proposals] [developers.uniswap.org] [Eco]

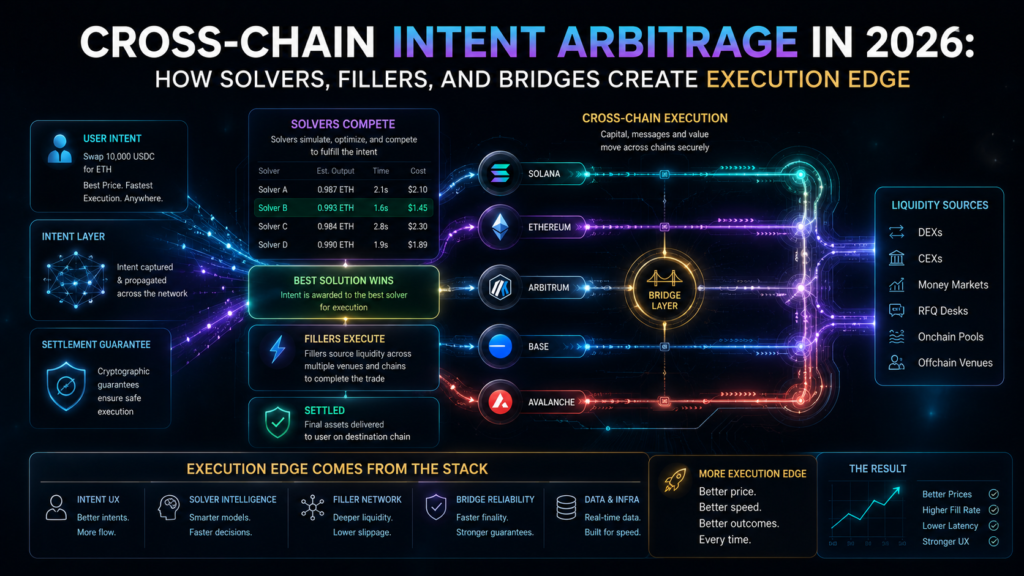

Cross-chain arbitrage in 2026 looks very different from the bridge-first playbook traders used even two years ago. The old approach was mostly mechanical: bridge asset A from chain X to chain Y, wait for finality, swap manually, and hope the spread survived latency, fees, and slippage. The new approach is intent-first. Instead of specifying every transaction step, the trader or application expresses the desired outcome, and a competitive network of solvers or fillers decides how to deliver it. That shift moves the edge away from raw route-following and into pricing, inventory management, auction logic, bridge selection, and settlement design.

In practical terms, cross-chain intent arbitrage means profiting from the gap between what a user wants done and the cheapest, fastest, safest way to get it done across multiple chains. The solver that can source liquidity better, internalize flow, net opposite directions, and rebalance more intelligently can capture spread that a slower participant never sees. That is why the execution edge in 2026 belongs less to the trader who finds a public spread and more to the solver stack that can monetize it before the market compresses.

What cross-chain intents actually change

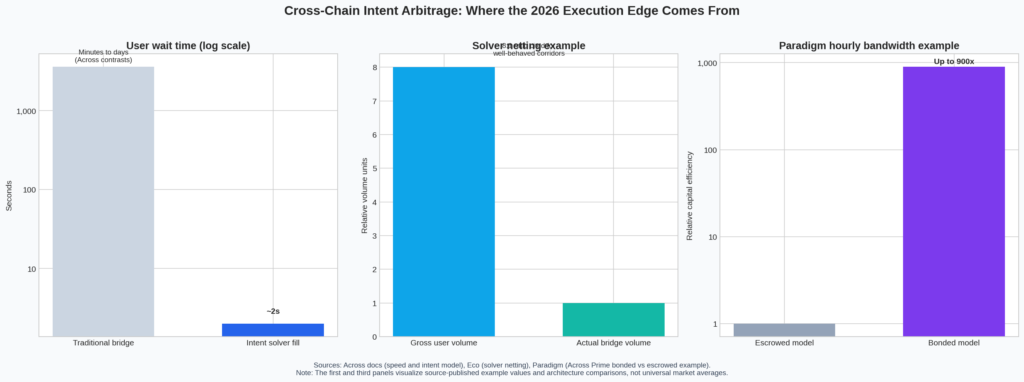

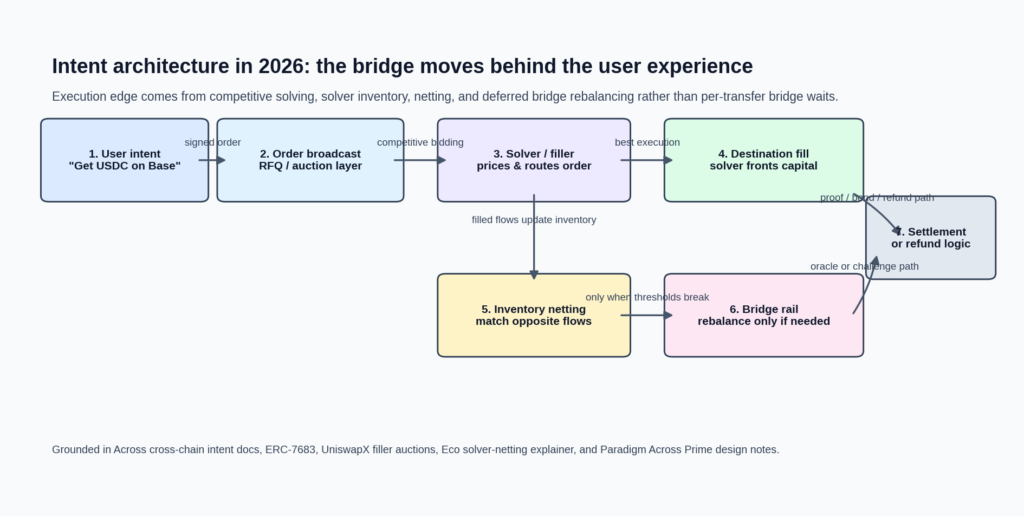

A cross-chain intent flips the UX and execution model. Rather than telling the protocol, “lock here, message there, mint there, then swap there,” the user says, “I want 100 USDC on Base,” or “swap my ETH on Arbitrum for at least 2,000 USDC on Base and send it to this address.” Across describes this as outcome-based execution, where solvers bear routing complexity instead of the user. Across also contrasts traditional bridge latency of minutes to days with intent-based fills that can arrive in roughly two seconds when the solver fronts capital on the destination chain.

That distinction matters because arbitrage economics are dominated by time. A spread that looks attractive in a spreadsheet often disappears during canonical bridge finality, intermediary swaps, or gas spikes. Intent systems compress that uncertainty window. If a professional solver can fill immediately from local inventory, then hedge, net, or rebalance later, the user-facing transaction becomes faster and often cheaper, while the solver captures the difference between quoted execution and actual backend cost.

Why ERC-7683 matters for arbitrage desks

One of the biggest bottlenecks in early intent systems was fragmentation. Every protocol had its own payload formats, settlement assumptions, and payment semantics, which meant each solver needed bespoke integrations. ERC-7683 directly targets that problem by standardizing the solver-facing representation of cross-chain orders. The point is not to force every protocol into one escrow contract or one settlement design, but to make order consumption more portable so solvers can support more intent flow with less custom engineering.

For arbitrage desks, that is a structural edge. Standardization lowers integration costs, improves order portability, and increases the odds that profitable flow gets routed into a broader competitive network rather than trapped inside a protocol silo. In other words, ERC-7683 is not just a developer convenience layer. It is part of the market microstructure that determines how much competition exists at execution time and how quickly solver liquidity can move to the best-paying opportunities.

Solvers vs fillers vs bridges: who does what?

The terms get used interchangeably, but there are useful distinctions. A solver is the actor or system that evaluates an intent, prices the risk, determines the route, and decides whether the order is economically viable. A filler is the participant that actually settles or submits the winning execution path. In some systems the same entity does both; in others the roles are partially separated by auction design or network architecture. UniswapX, for example, describes fillers as specialized participants that monitor signed orders and compete to settle them using their own liquidity or external liquidity sources.

The bridge used to be the product. In 2026 it is increasingly the rail. That is a huge difference. In solver-centric architectures, the bridge is no longer the primary interface where the user waits, pays, and takes execution risk. Instead, the bridge becomes a back-end mechanism the solver uses for inventory rebalancing, settlement proof, or delayed fund movement. Eco’s solver-netting explanation makes this explicit: the economic win is not that bridges disappear, but that user-facing latency and cost become decoupled from the bridge’s own latency and cost.

Where the new execution edge actually comes from

The first source of edge is inventory. A solver with balanced stablecoin inventory on Ethereum, Arbitrum, Base, Optimism, and Solana does not need to bridge every user transaction in real time. It can pay out locally, then rebalance when the aggregate imbalance justifies it. That alone can turn a slow, fee-heavy path into a near-instant fill, especially in stablecoin-heavy corridors where flow naturally offsets.

The second source is auction design. UniswapX shows why. Users sign an order, fillers compete, and the winning fill depends on when the order becomes economically viable within the auction timeline. That means execution quality is shaped by who has the best routing, the best private liquidity access, the best gas strategy, and the fastest response loop. In a world of public spreads, auction mechanics and private inventory matter more than naive opportunity detection.

The third source is solver netting. Eco describes solver netting as matching opposing cross-chain intents on the solver’s own balance sheet so the underlying funds rarely need to move across a bridge immediately. The article notes that in well-behaved bidirectional corridors the netting ratio can exceed 8:1, meaning gross user volume may settle with only one-eighth of the actual cross-chain transfer volume. That is a profound arbitrage advantage because it compresses bridge fees, lowers operational drag, and lets solvers batch rebalances when conditions are cheaper.

The fourth source is settlement architecture. Paradigm’s analysis of Across Prime is especially important here. In a classic escrowed model, the user’s payment sits locked until fulfillment is verified, which creates real capital cost for relayers. Across Prime proposes a bonded model where the relayer receives payment immediately and user safety is backed by the relayer’s security deposit. Under Paradigm’s illustrative assumptions, that bonded structure can produce up to 900x greater hourly bandwidth than the escrowed alternative. Even if real-world performance varies, the design lesson is clear: whoever can reduce idle capital and settlement drag can quote tighter execution.

The fifth source is bridge abstraction. Once the bridge becomes a rebalancing rail rather than a per-transaction dependency, the solver can choose the cheapest rail at the right time. Eco explicitly frames bridges such as CCTP, LayerZero OFT, Hyperlane, or canonical bridges as back-end mechanisms triggered only when inventory thresholds are crossed. That is exactly where professional desks create edge: they transform bridge selection from a user problem into a treasury optimization problem.

Why this matters for crypto arbitrage in 2026

For traders, this means “finding the spread” is no longer enough. The visible price discrepancy is often the least interesting part of the trade. The harder and more valuable problem is execution: can you fill instantly, source the right liquidity, net against opposite flow, hedge residual inventory, and settle without tying up too much capital? If not, someone with a stronger solver stack will compress your margin away.

For builders, it means the best product experience increasingly comes from hiding bridge complexity behind intents. Across openly positions this shift as removing routing, finality, and bridge complexity from the end user. That is not just good UX. It is good market design because it increases the number of executable orders and invites more solver competition around them.

For AI-driven arbitrage platforms like NeuralArB, the opportunity is obvious. NeuralArB’s own positioning emphasizes ultra-low-latency infrastructure, large-scale real-time market data processing, and adaptive execution logic for arbitrage. Those capabilities map naturally onto a 2026 intent market where the edge comes from routing intelligence, latency compression, inventory awareness, and automated risk control rather than static bridge scripts.

The risks most articles skip

This new architecture is not free money. Solver systems introduce new forms of operational concentration, inventory risk, and settlement complexity. If you quote too tightly and your inventory goes one-way, the rebalance can erase the spread. If you rely on one bridge rail and it degrades, your model can become directionally exposed fast. If your auction participation is slow, you only win toxic flow. If your settlement assumptions are wrong, capital efficiency gains can turn into insolvency risk.

There is also the standardization risk. ERC-7683 reduces fragmentation, but adoption depth and implementation quality still matter. A standard can widen access to order flow, yet real execution remains path-dependent on resolver quality, oracle assumptions, chain-specific auction dynamics, and available liquidity. In short, standardization creates a larger playing field, not a guarantee of easy profits.

How serious desks should think about execution edge now

The best way to think about cross-chain intent arbitrage in 2026 is as a balance-sheet and systems problem, not merely a pricing problem. A modern desk should model corridor-level inventory, chain-specific gas regimes, quote decay, solver hit rate, rebalance thresholds, and settlement latency as one integrated system. That is where repeatable edge comes from. Public spread scanners are table stakes; solver economics are the real moat.

That is also why the market is moving toward intent-native execution stacks. The protocols that win will be the ones that attract dense order flow and broad solver competition. The desks that win will be the ones that combine low-latency execution, capital-efficient settlement, and AI-driven route selection into a single operating layer. NeuralArB’s broader editorial focus on AI arbitrage, cross-chain MEV, and routing efficiency already fits that narrative well.

📥 Download the supporting assets – Cross-Chain Intent Execution Edge 2026

💬 Frequently Asked Questions (FAQ)

What is cross-chain intent arbitrage?

Cross-chain intent arbitrage is the process of capturing execution or pricing edge by expressing a desired result across chains and letting solvers or fillers compete to deliver it more efficiently than a manual bridge-and-swap path.

What is the difference between a solver and a filler?

A solver evaluates an intent, prices it, and determines whether and how to execute it. A filler is the participant that actually settles the order, often using its own liquidity or a chosen route. In many systems one entity performs both roles, but the conceptual split helps explain where the economics sit.

Are bridges becoming obsolete?

No. Bridges are becoming less visible to end users, but more important in the background. In solver-centric systems, the bridge is typically used for rebalancing, settlement verification, or delayed inventory movement rather than for every user-facing transaction.

Why is ERC-7683 important?

ERC-7683 reduces fragmentation by standardizing how solvers consume cross-chain intent orders. That lowers integration overhead and can increase competition among solvers, which may improve execution quality over time.

How does solver netting improve profitability?

Solver netting lets a desk match opposite-direction flows internally, reducing the amount of actual bridge traffic needed. That lowers fees, reduces latency pressure, and improves capital efficiency because not every user order needs immediate cross-chain settlement.

Why do auction-based systems matter for arbitrage?

Auction-based intent systems matter because the winner is not just the trader who sees the opportunity first, but the participant who can price and execute it best. Fillers compete using their own inventory, routing logic, and external liquidity access, which makes execution capability the core advantage.

What is the biggest mistake desks make in cross-chain arbitrage?

Treating bridge latency and settlement as afterthoughts. In 2026, execution edge depends heavily on inventory placement, solver response times, settlement design, and the ability to rebalance cheaply after the user-facing fill. www.paradigm.xyz

If you want to compete in the next phase of crypto arbitrage, you need more than spread alerts and basic bridge scripts. You need infrastructure that can monitor fragmented liquidity, adapt across chains, and execute with speed and discipline.

NeuralArB is built around that thesis: AI-powered arbitrage, low-latency market intelligence, and smarter routing for traders who want execution edge beyond static bots.

Explore the platform, audit your current cross-chain workflow, and start building an intent-native trading stack before manual routing becomes the slowest layer in your system.

Disclaimer: These materials are for general information purposes only and are not investment advice or a recommendation or solicitation to buy, sell or hold any cryptoasset or to engage in any specific trading strategy. Some crypto products and markets are unregulated, and you may not be protected by government compensation and/or regulatory protection schemes. The unpredictable nature of the cryptoasset markets can lead to loss of funds. Tax may be payable on any return and/or on any increase in the value of your cryptoassets and you should seek independent advice on your taxation position.